15 Thoughts on Berkshire Hathaway's 2024 Proxy Statement

I've got lots to say (what else is new) on Berkshire's board of directors, share repurchases, executive compensation, puzzling shareholder proposals, and more...

Happy Monday and welcome to our new subscribers!

Special thanks, too, to those who recently became paid supporters! ❤️

As expected, Berkshire Hathaway released its annual proxy statement on Friday afternoon. And, while some people’s eyes might glaze over at the prospect of reading another SEC filing, I actually find the proxy to be one of the more enjoyable entries in this all-too-often-boring genre.

It contains lots of information on Berkshire’s board of directors, executive compensation, shareholder proposals, and other relevant details ahead of the upcoming shareholders meeting in May. And, blessedly, Warren Buffett and co. always keep the corporate jargon and legalese to a bare minimum.

This accessibility is important because Berkshire’s proxy actually tells us a whole lot about the company — and how Buffett and Munger assiduously built it in their image. A conglomerate unusually focused on ethical dealing, an attitude of partnership with its shareholders, and a unique culture that will hopefully persist for decades to come.

Still, not everyone wants to spend St. Patrick’s Day weekend poring over an SEC filing.

I get that.

So, in the spirit of public service, I’ve gone through the proxy with a fine-tooth comb and pulled out all of the most important details and information. And, to the best of my abilities, tried to summarize it all in plain English. I hope it proves helpful.

(1) Not every board of directors is created equal. Is it a sinecure to enrich powerful friends with extravagant perks and lucrative fees? Or, instead, a like-minded group of industrial exemplars who care deeply about the company’s future — while pledging to represent the shareholders’ interests at every turn?

In other words: Are the directors only out for themselves or are they proud stewards of that particular company’s culture and vision?

Happily, at Berkshire Hathaway, it’s very much the latter.

(2) How does Berkshire find the right people for this crucial role? The proxy states that Berkshire “looks for individuals who have very high integrity, business savvy, an owner-oriented attitude, a deep genuine interest in Berkshire, and have had a significant investment in Berkshire shares relative to their resources for at least three years. These are the same attributes that Warren Buffett … believes to be essential if one is to be an effective member of the Board of Directors.”

(3) One thing is clear: It’s not about the money. At many large companies, joining the board of directors comes along with a fat paycheck. Not so at Berkshire, though, where non-employee directors receive just $900 for each in-person meeting and $300 for each phone meeting. Members of the Audit Committee also get $1,000 per quarter.

And that’s it.

“I like that Berkshire doesn’t pay its directors in any meaningful way,” Chris Davis recently told the Excess Returns podcast, “because it reinforces that you’re there out of a sense of duty.”

(4) Warren Buffett insists that his board of directors have sufficient “skin in the game” to align their own financial interests with those of the shareholders. He makes no secret of the fact that he expects every Berkshire director to invest a sizable portion of his or her own money into the company’s stock.

Notice I said “his or her own money”. Shares are never handed out at Berkshire. Not to employees, not to directors, not to Warren Buffett himself. No one is above that law.

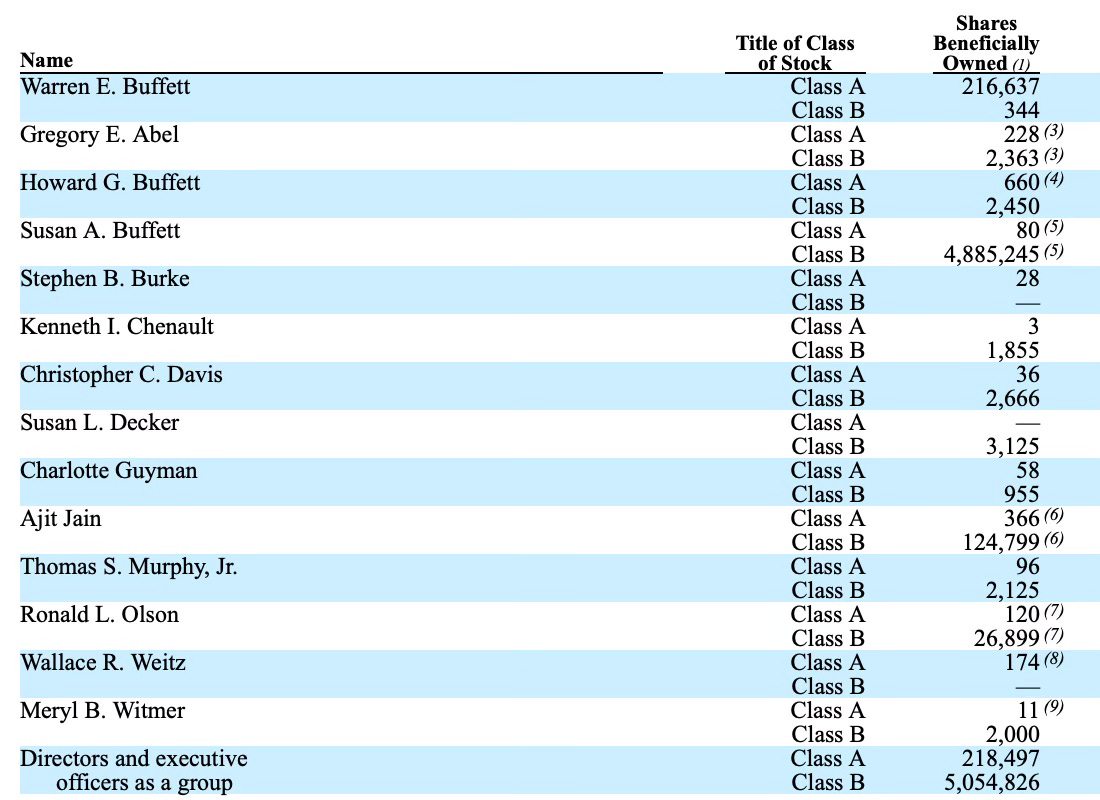

Here is how the fourteen members of the board stack up in terms of shares owned:

(5) And, now, ranked by the current financial value of their Berkshire holdings:

Warren Buffett: $133.9 billion

Susan Buffett: $2.04 billion

Howard Buffett: $408.9 million

Ajit Jain: $277.2 million

Greg Abel: $141.9 million

Wallace Weitz: $107.6 million

Ronald Olson: $85.2 million

Tom Murphy Jr.: $60.2 million

Charlotte Guyman: $36.2 million

Christopher Davis: $23.3 million

Stephen Burke: $17.3 million

Meryl Witmer: $7.6 million

Kenneth Chenault: $2.6 million

Susan Decker: $1.3 million

(Note: A significant portion of Howard and Susan Buffett’s holdings are in their respective charitable foundations. Wallace Weitz, too.)

(6) Before anyone takes up torches and pitchforks against the names at the bottom of this list, remember that the proxy only asks for “a significant investment in Berkshire shares relative to their resources”.

And, as the proxy also states, “In the judgment of the Governance Committee, as well as that of the Board as a whole, each of the candidates being nominated for director possesses such attributes.”

When it comes to calculating net worths and determining what percentage ought to be invested in Berkshire stock, I will defer to Warren Buffett. If he’s happy, I’m happy.

That being said, directors of a public company — let alone one as prestigious as Berkshire — must be cognizant of PR. If I were down towards the bottom of that list, I think I would buy more shares (especially vote-rich Class A shares) at the earliest opportunity and eliminate that source of shareholder grumbling.

(7) Berkshire has really ramped up share repurchases over the past month. While most of the proxy is devoted to the board of directors, executive compensation, and annual meeting details, the company also kindly provides an updated share count (as of March 6, 2024). And, from that, we can see that Buffett has been busy.

Between February 12 and March 6, Berkshire repurchased 2,813 Class A equivalents to bring its total on the year to 3,808 shares. That means Buffett has already shelled out approximately $2.3 billion on repurchases in Q1 2024 — with several weeks still to go. (That also means that he has already eclipsed last quarter’s outlay of $2.2 billion.)

(8) Greg Abel and Ajit Jain received raises in 2023. Warren Buffett, as usual, did not. Last year, both vice chairmen earned $20 million in base compensation — a 5% increase over 2022 ($16 million base plus $3 million bonus).

Unlike at most companies, top executives like Abel and Jain receive no stock-based compensation at Berkshire. That’s just not how things are done there. If they want to purchase Berkshire stock — and, as directors, Buffett strongly encourages it — they’ll need to use their own paychecks to do so. No dilution for current shareholders and a big financial commitment from the executives in question.

Buffett, meanwhile, plodded along with the same $100,000 salary that he has had for the last 35 years. It’s safe to say that he’s just a wee bit underpaid.

(9) At Berkshire, meritocracy is the name of the game. “Berkshire does not have a policy regarding the consideration of diversity in identifying nominees for directors,” the proxy states. “In identifying director nominees, the Governance Committee does not seek diversity, however defined.” The qualifications — stated above in #2 — are always the same for everyone. Long may that continue.

Become a paid supporter today and receive immediate access to eight (and counting) annotated transcripts full of wit and wisdom from the top names at Berkshire Hathaway.

Paid subscribers will also continue to receive a new annotated transcript each month.

(10) In order to thrive, you must first survive. In addition to his other titles and responsibilities, Warren Buffett serves as Berkshire’s chief risk officer. Always considering and contemplating what could go wrong with his subsidiaries and investments — and never losing sight of the fact that many Berkshire shareholders keep an unreasonable percentage of their net worth invested in the company.

(11) The estate of Walter Scott, the late Berkshire director, continues to own approximately 8% of Berkshire Hathaway Energy. As the matter currently stands, Berkshire retains first dibs on the Scott estate’s BHE stake if it is ever put up for sale. Likewise, the Scott estate can “put the shares” to Berkshire at any time — and receive its payment in Berkshire stock.

(12) Insurance remains a critical component of the Berkshire machine. Berkshire’s insurance operations, expertly managed by Ajit Jain, fueled much of the company’s strong performance in 2023. As such, I really liked this passage from the proxy: “The primary business of Berkshire’s insurance operations is to monitor, assess, and price risk at an expected economic profit to address the risk-transfer needs of its insurance customers. If there were no risks, or all risks were assumed by governments, there would be no insurance business.”

“Berkshire has no idea what loss costs will be for autos 10, 20, or 30 years from now. That’s why it generally sells only six-month policies. This same caution in respect to future loss costs applies to all property/casualty coverages. To date, Berkshire has been quite successful in matching prices to risk, and 2023 was a particularly good year.”

(13) RIP Charlie Munger. The proxy does not mention when — or if — the late Charlie Munger will be replaced on Berkshire’s board. But, in a sad reminder of his absence, the last sentence in the “Risk Oversight” section mistakenly refers to “Berkshire’s three Vice Chairmen”. A club that now, sadly, numbers only two.

(14) Chris Davis has emerged as an outspoken defender of Berkshire’s culture. And, hopefully, an immovable bulwark against institutional creep in the post-Buffett era.

“Berkshire has been unconventional enough that I can imagine all sorts of people coming out of the woodwork [after Warren and Charlie are gone] with shareholder proposals to unlock short-term value at the expense of long-term value,” he said recently. “It will be the job of the board to protect that culture.”

Well, on that front…

(15) Six shareholder proposals will come up for a vote on May 4 — and Berkshire would like to see all six go down in flames. It’s the usual coterie of ESG stuff — with one about railroad safety thrown in, too, that mistakenly believes that BNSF uses Precision Scheduled Railroading. (It doesn't.)

I’ll leave it up to each of you to reach your own conclusions on these shareholder proposals and their respective merits (or lack thereof), but Berkshire’s position is clear: No dice. Agreeing to any of the six would betray and destabilize the conglomerate’s carefully-constructed decentralized structure.

To me, the answer to anyone agitating for change is a simple one. Why mess with a good thing?

The Rational Walk, reckons that 253,300 Class A shares traded in 18 days this year which is half of all outstanding class A's. What am I missing?

Has there actually been shareholder grumbling about Ken Chenault and Susan Decker's stock holdings not being adequate?