What Does Berkshire Hathaway See in Snowflake?

SBC, much like SBF, is the silent killer of investment returns

Happy Friday and welcome to our new subscribers!

Scanning through the list of Berkshire Hathaway’s massive investment portfolio, the vast majority of holdings fit right in with Warren Buffett’s value-based approach. Lots of strong brand names — or franchises — with predictable profits and cash flow.

A few companies, though, stick out like sore thumbs as distinctly un-Berkshire-like. (Snowflake and StoneCo, I’m looking at you.)

That doesn’t make them bad investments or call into question the acumen of Buffett and his investing lieutenants, but it does pose the question: Why did Berkshire buy these stocks in the first place?

If nothing else, I try to use every opportunity that I can find to learn more about Buffett and Berkshire’s process on my way to becoming a more intelligent investor. (And, believe me, I’ve got miles to go before hitting that goal…)

Today, Snowflake goes under the microscope.

Berkshire bought 6.1 million shares of SNOW 0.00%↑ at its IPO in 2020. Snowflake provides a consolidated cloud-based data platform to customers worldwide with a particular emphasis on efficiency and analysis.

And, as you might expect from a cloud-based newcomer, Snowflake had no earnings and traded at a pretty steep valuation (price-to-sales ratio of approximately 60) at the time of its IPO.

Like I said, this one was a bit out of character for Warren Buffett and co.

Wait, Berkshire bought Snowflake at its IPO?

Warren Buffett has always been a vocal critic of buying IPOs.

Though, in this case, it almost certainly was not Buffett snapping up these shares of Snowflake. (More on that in a minute.)

At the 2012 annual shareholder meeting, he said:

The idea that somebody is bringing something to market today, a seller who has a choice of when to come to market, and that that security, where there’s going to be a lot of hoopla connected with it, is going to be the single cheapest thing to buy out of thousands and thousands and thousands of businesses in the world is nonsense.

Later that day, he re-emphasized the point:

You know it can’t be the most attractive thing, but people get excited about what’s coming and all that sort of thing.

But I will guarantee you that if you have thousands of opportunities among stocks all over the world and most of them are not being promoted or being sold with special commissions in them or something else, and then some other security is coming to market that day, when the seller picks the time to bring it, as opposed to just this auction market operating otherwise, it just doesn’t make sense to spend five minutes thinking about new issues.

So we don’t think about them.

Berkshire buying Snowflake notwithstanding, Buffett makes a sound argument.

Companies pull the trigger on an IPO when they feel that they can make the most money selling shares to the public. For any investor who prefers to pounce on market inefficiency and irrational pessimism, IPOs aren’t it. Much like a Billy Mumphrey story, they’re all about unbridled enthusiasm.

Berkshire sidestepped one of the main perils of the IPO process — a frenetic first day that shoots the stock price to the moon — by purchasing its 6.1 million shares ahead of time for the stated $120 price.

And it’s a good thing that they did — Snowflake gained 112% on IPO day.

In 2019, Buffett told Becky Quick: “Buying new offerings during hot periods in the market, I don’t think is anything the average person should think about at all.”

While Berkshire did fine at Snowflake’s IPO — owing to its ability to lock in millions of shares at $120 — the average individual investor would have gotten slaughtered buying on the open market as the price soared into the mid-$250s.

So who did the buying?

While we can never be absolutely certain about who called the shots on Snowflake — that is, unless someone at Berkshire starts talking — the lion’s share of the evidence points to Todd Combs.

GEICO (where Combs serves as CEO) uses Snowflake’s cloud-based data services, giving him a close-up look at how the company operates and its various competitive advantages.

Plus, Snowflake CEO Frank Slootman once revealed that Combs was frequently in touch with him around the time of the IPO and expressed an interest in investing.

I don’t think it takes Sherlock Holmes to puzzle this one out.

On a somewhat unrelated note, Slootman also told a story about how Combs operates at GEICO. The managerial aspect of Combs’s work at Berkshire doesn’t typically get a lot of attention, so it’s rather nice to gain some insight into that side of him.

I remember being with GEICO CEO Todd Combs, who has also become an investor at Snowflake.

Talking to him, he was like, “Look, I don’t want to hear anything about your architecture or what a great platform [you have]. I believe all that. Check. Let’s move on to real problems that I have in the business. For example, we have much higher bodily injury claims in Florida and in surrounding states and I don’t know why that is. You have one week to come in here and tell me how the product works in terms of solving those kinds of issues.”

One week.

We’re like on our heels because we know nothing about insurance. But that’s how you create energy and pressure and focus. Hell, that changed our whole company’s focus.

Slootman credits Combs’s down-to-business attitude with re-aligning Snowflake’s focus in a new direction. And Snowflake, in turn, must have impressed Combs with whatever solutions they presented — leading him to invest in the company.

What does Warren Buffett think about Snowflake?

The real answer is that it doesn’t matter. Buffett completely trusts and empowers Ted and Todd to make their own investment choices according to their own convictions with the funds given to them. Combs did not need his boss to sign off before buying those 6.1 million shares of Snowflake in 2020.

But, understandably, everyone always wants to know what Buffett thinks about a particular company or investment. That just comes with the territory when you’re the investing GOAT.

On many levels, Snowflake is the antithesis of a Buffett stock. Typically, Buffett would run screaming from an IPO without earnings based in the fiercely competitive tech industry.

It’s pretty safe to assume that he would not have bought Snowflake on his own.

But here’s a caveat to that statement: Buffett has often lamented that Berkshire missed out on Google, even though he had a front-row seat (through GEICO) to the power of online advertising and Google’s iron grip on that field.

From the 2019 annual shareholder meeting:

Munger: I feel like a horse’s ass for not identifying Google better. I think Warren feels the same way.

Buffett: Yeah.

Munger: We screwed up.

Buffett: He’s saying we blew it. (Laughs) And we did have some insights into that because we were using them at GEICO. We were seeing the results produced. We saw that we were paying $10 a click, or whatever it might’ve been, for something that had a marginal cost to them of exactly zero. And we saw it was working for us.

Munger: We could see in our own operations how well that Google advertising was working. And we just sat there sucking our thumbs. (Laughs) So, we’re ashamed. We’re trying to atone.

Let’s be clear: I’m not comparing Snowflake to Google.

But GEICO’s exposure to Snowflake, just like Google before it, might have given Berkshire some keen insights into the company’s future prospects. And, after missing out on Google, maybe Buffett felt more willing to take a flyer on something like Snowflake.

I wouldn’t bet on that being the actual explanation, but it’s an interesting parallel.

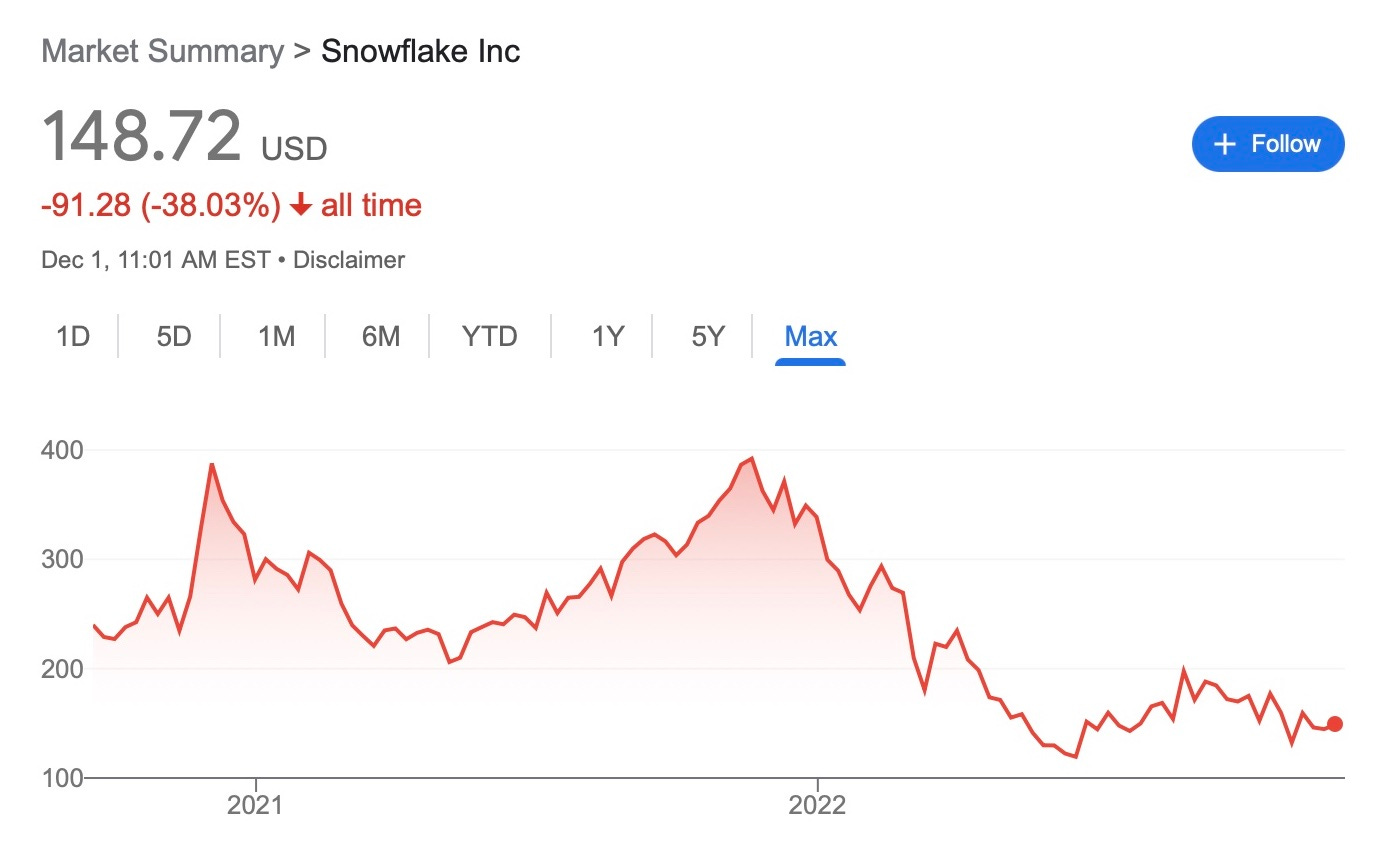

How does Snowflake look today?

Snowflake’s story hasn’t changed much since its IPO: Strong revenue and customer growth. Operating losses. And mounting stock-based compensation.

When Berkshire first invested in Snowflake, it owned 2.2% of the data cloud company. But, due to high levels of stock-based compensation, that stake has been noticeably diluted in just two years.

SBC, much like SBF, is the silent killer of investment returns.

And, despite Snowflake being one rollercoaster ride of a stock, Berkshire Hathaway gives every indication of sticking it out for the long haul.

I may not understand it, but Todd Combs has had plenty of opportunities to get out of Snowflake at a healthy profit and instead chooses to hold.

Another early investor, Salesforce, cashed out of SNOW 0.00%↑ in 2021 at a likely price of over $200 per share. Time will tell whether Combs or Salesforce made the better choice.

If nothing else, Berkshire’s continued faith in Snowflake suggests that its investing thesis for the company remains in place. I just hope that by the time Snowflake becomes profitable — whenever that is — Berkshire’s stake hasn’t been diluted away.

If you’ve enjoyed reading this issue of Kingswell, please hit the ❤️ below and share it with your friends (and enemies) so they don’t miss out. It only costs you a few clicks of the mouse, but means the world to me. Thank you!

Disclosure: This is not financial advice. I am not a financial advisor. Do your own research before making any investment decisions.

Great post, i like what you write and your style. Keep it up. My sense is that Combs is a bit overrated, perhaps I am wrong, but he is doing many things at the same time and few are not working well so far.

Larry and Sergey met with Warren Buffett to ask his advice on a dual class structure pre ipo. So I can see why Buffett feels like he missed out given the direct experience as a customer and knowing these brilliant guys personally!