The New Kids on Berkshire's Block: Q3 2022 Edition

Quick hits on TSMC, Louisiana-Pacific, and Jefferies Financial Group

Happy Monday and welcome to our new subscribers!

I’m not finished with last week’s 13F quite yet.

Today, let’s take a closer look at the three companies that joined Berkshire Hathaway’s investment portfolio for the first time in Q3 2022.

But, first, it’s nice to know that Berkshire can still move the market…

Taiwan Semiconductor Manufacturing Co.

Shares: 60.1 million

Current Value: $4.94 billion

Some question whether or not this is a Warren Buffett pick, but I think TSMC fits right into his investing wheelhouse. The world’s largest contract chipmaker boasts unparalleled infrastructure — and a client list to match — that makes it nigh impossible for the competition to wrest away market share.

Berkshire expert Christopher Bloomstran agrees. “I don’t think [TSMC] is outside Warren’s circle of competence,” he told Barron’s. “Durable profitability, great balance sheet, and a high earnings yield. All characteristics of a Buffett investment.”

Add in a falling stock price and TSM 0.00%↑ ticks all the boxes of a classic Buffett play. Opportunities like this, with a gold-standard company selling at a low price, don't come around very often.

Last week, I noted that Buffett likely views TSMC akin to Apple. Obviously, not as a consumer brand — Apple inspires such loyalty and excitement that fans line up for hours ahead of every new iPhone launch. On the other hand, very few customers specifically demand that a product include a TSMC-made computer chip.

To the end user, semiconductors (at least from a manufacturing standpoint) are basically commodities. Switching from iOS to Android (or vice versa) is a very big deal, but who would even notice if their device used a TSMC chip instead of a Samsung one?

No one.

But TSMC gets its customers — companies like Apple, Nvidia, Qualcomm, and many others — to line up to use its massive foundries and advanced node technology. The Taiwanese giant excels at staying on the cutting edge of semiconductor design, outpacing rivals in creating smaller and smaller chips, while simultaneously offering effective yields and a huge amount of production capacity.

TSMC’s moat is different than Apple’s, but no less daunting to upstart competitors.

Owing to certain geopolitical uncertainties, some investors shy away from TSMC. A substantial portion of the company’s manufacturing infrastructure is located in Taiwan — and, for many, that’s putting too many eggs in one basket.

TSMC, though, has been working to allay these fears by diversifying globally. Work is already underway on a $12 billion plant in Arizona — plus some whispers that a second foundry, north of Phoenix, might be on the way — and new facilities are coming to Japan and (maybe) Germany, too.

Subsidies are flowing from both the United States and Europe — and TSMC aims to take advantage of that to move as much critical infrastructure out of China’s path as possible.

TSMC has lost approximately $240 billion in value this year. Mostly due to worries about cooling global demand for semiconductors.

But, even if the industry cycles down in 2023, the long-term prospects for computer chips remain white hot. You might have to zoom out a bit — depending on how difficult 2023 gets from an economic perspective — but this should easily be a trillion-dollar industry down the road.

And probably sooner rather than later.

Even if Samsung rights the ship and Intel pulls off its transition into a contract manufacturer, there will be plenty of money to go around for the top dogs. TSMC is growth and safety in one package.

Louisiana-Pacific Corp.

Shares: 5.8 million

Current Value: $357.4 million

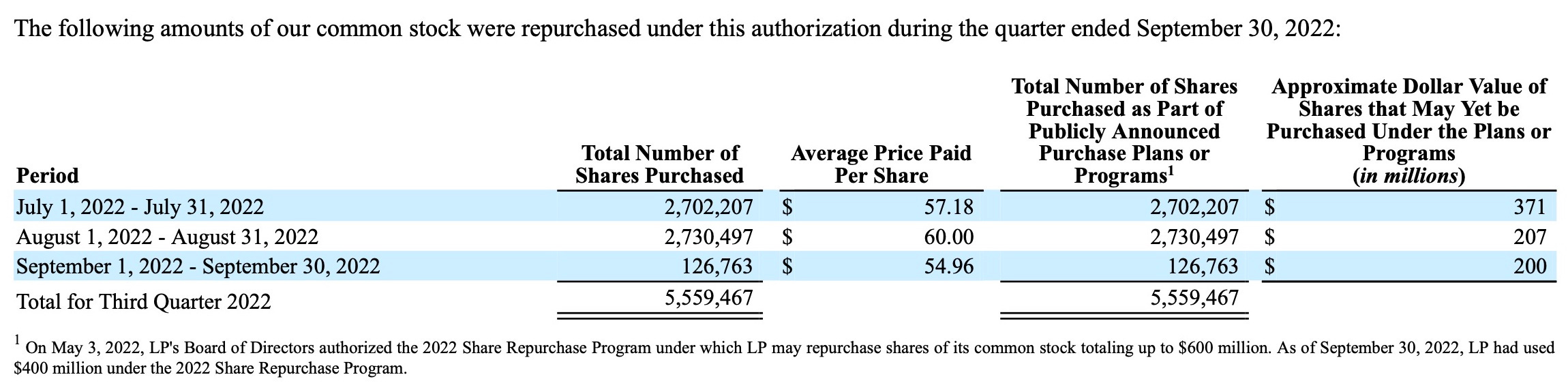

Louisiana-Pacific might be the most aggressive repurchaser of its own stock that I’ve ever seen. The Nashville-based building materials company spent $325 million to buy back 5.6 million shares in the third quarter.

That’s 7.2% of LP’s entire outstanding stock.

Repurchased in one quarter.

And that’s not an isolated incident. From 2018 to now, shares outstanding have dropped from 144 million down to 71.7 million. For the math-averse, that’s over half of the company. Bought back in less than five years.

Recently, though, the pace of buybacks has slowed to a crawl. Between September 30 and October 31, LP’s shares outstanding only dropped from 71.7 million to 71.695 million. Despite LPX 0.00%↑ spending most of the month in the mid-$50s, where management had previously been an eager repurchaser.

Louisiana-Pacific still has $200 million left in its authorized share repurchase program, so this recent shift in strategy remains a bit of a mystery.

Warren Buffett is a big fan of buybacks.

“The process offers a simple way for investors to own an ever-expanding portion of exceptional businesses.”

Though he’s pretty critical of how many turn out in practice.

“American CEOs have an embarrassing record of devoting more company funds to repurchases when prices have risen than when they have tanked.”

Buying back shares when prices are high — and avoiding them when cheap — is the exact opposite of effective capital allocation. And there are shades of that at Louisiana-Pacific.

As you can see, LP repurchased 2.7 million shares in both July and August at an average price of $57.18 and $60 respectively. But in September, when prices dropped to $54.96, the company only bought back 126,000+ shares. Not ideal.

Louisiana-Pacific x Clayton Homes. On Twitter, @nopain_n0gain86 pointed out a connection between LP and Berkshire-owned Clayton Homes. At Berkshire’s annual meeting this year, LP was featured as the trim and siding partner for Clayton’s first net-zero electricity home.

“One of our core values at LP is doing the right thing today to ensure a brighter future for the next generation,” said executive vice president Jason Ringblom, “and we are committed to building relationships with companies who value the same.”

Jefferies Financial Group

Shares: 433,558

Current Value: $16.3 million

In a quarter where Berkshire cut back on two long-time financial holdings — U.S. Bancorp and Bank of New York Mellon — Warren Buffett and co. found room to add Jefferies to the mix.

Just not very much of it.

A $16 million position might sound like a lot to us mere mortals, but it’s exceptionally tiny by Berkshire standards. JEF 0.00%↑ won't move the needle. (Unless Berkshire buys more in Q4.)

Jefferies, formerly known as Leucadia, has a long history with Berkshire Hathaway. In 2009, the two companies teamed up to purchase mortgage servicer Capmark Financial and transformed it into the creatively-named Berkadia. At a time when the rest of the market was fleeing the fiery wreckage of the mortgage biz, Berkshire and Leucadia snapped up a nice package of assets at a very attractive price.

Both companies share in the profits from this commercial mortgage venture — $238 million of cash earnings in 2021 — but Berkshire has also found other ways to monetize Berkadia.

At first, Berkshire collected interest on a $1 billion credit facility that it extended to the mortgage servicer. And, now, a Berkshire subsidiary insures the commercial paper that Berkadia uses to fund its operations.

Even on a smallish project like this, Warren Buffett finds a way to minimize risk and collect cash during good times and bad.

If you’ve enjoyed reading this issue of Kingswell, please hit the ❤️ below and share it with your friends (and enemies) so they don’t miss out. It only costs you a few clicks of the mouse, but means the world to me. Thank you!

Disclosure: This is not financial advice. I am not a financial advisor. Do your own research before making any investment decisions.