The Berkshire Beat: September 15, 2023

All of the latest Berkshire Hathaway news and my must-reads of the week!

Happy Friday and welcome to our new subscribers!

Special thanks, too, to those who recently became paid supporters! ❤️

The latest news and notes out of Omaha…

It’s been a banner week for Berkshire Hathaway. On Monday — for the first time ever — Berkshire closed the day with a market cap over $800 billion. According to the Wall Street Journal, that marked a new record for the company — topping the previous high of $794 billion in March 2022. And it hasn’t stopped there. At last check, Berkshire’s market cap had zoomed up to $813 billion.

Berkshire’s Class A ($562,481) and Class B ($370.84) shares both hit new all-time intraday highs this week, too.

And, after trailing the benchmark index for most of the year, Berkshire has finally pulled ahead of the S&P 500’s year-to-date total return.

Class A: +19.85%

Class B: +19.62%

S&P 500: +18.74%

Between September 11-13, Berkshire sold 5.5 million shares of HP for approximately $158.4 million — reducing its stake in the tech company from 12.2% to 11.7%. HPQ 0.00%↑ has not been one of Berkshire’s more successful investments, declining by about 20% since April 2022. Let’s see if there are any more HP sales in the days to come.

🤑 On Monday, Berkshire received $185.9 million in quarterly dividends from Chevron. (Assuming, of course, that Warren Buffett did not sell any more shares in the first half of Q3…) Despite paring back on CVX 0.00%↑ over the last three quarters, Berkshire still owns 6.5% of the oil major — a position currently valued at $20.5 billion.

Berkshire also collected $1.98 million in dividends from GM yesterday.

Warren & Charlie received a shoutout in the new Howard Marks memo — Fewer Losers, or More Winners?: “Warren Buffett — arguably the investor with the best long-term record (and, certainly, the longest long-term record) — is widely described as having had only twelve great winners in his career. His partner, Charlie Munger, told me the vast majority of his own wealth came not from twelve winners, but only four.”

More from Marks: “I believe the ingredients of Warren’s and Charlie’s great performance are simple: a lot of investments in which they did decently, a relatively small number of big winners that they invested in heavily and held for decades, and relatively few losers. No one should expect to have — or expect their money managers to have — all big winners and no losers.”

I highly recommend the recent profile of Li Lu in the Financial Times — not least because Charlie Munger drops a number of great lines about his longtime friend:

On the apparent tension between Li’s past (a student leader at Tiananmen Square) and his present (a money manager with big investments in China): “Li Lu is no longer a revolutionary. He’s a capitalist. You can’t find a more capitalistic capitalist than Li Lu.”

Note to self: My new life goal is to have someone describe me as “a capitalistic capitalist”.

Munger added: “I’m not interested in revolution. I’m a capitalist. It was [Li Lu’s] capitalist attitude that attracted me, not his revolutionary history.”

On BYD: “It’s difficult to make a fortune in the auto business. [Li Lu’s] early investment in BYD was a minor miracle.”

Once upon a time, Munger hoped that Li Lu would run Berkshire’s investment portfolio in the post-Buffett era. But the Chinese-American investor chose to remain at Himalaya Capital and paint his own masterpiece. “He so liked being a principal instead of being an agent working for somebody else … That’s how I am, so I had considerable sympathy for him. I tried to get him to work at Berkshire, but I was fighting against [his] nature.”

Earlier this week, Occidental Petroleum — through its 1PointFive subsidiary — agreed to sell 250,000 metric tons of carbon removal credits to Amazon over the next ten years. These credits will come from the STRATOS Direct Air Capture (DAC) facility currently being built in Texas.

Michael Avery of 1PointFive: “Amazon’s purchase and long-term contract represent a significant commitment to direct air capture as a vital carbon removal solution.”

An interesting comment from Oracle co-founder Larry Ellison on this week’s ORCL 0.00%↑ Q1 2024 earnings call: “I’m now able to announce that all nine utility companies owned by Berkshire Hathaway are in the process of replacing all of their existing [enterprise resource planning] systems and standardizing on Oracle’s Fusion Cloud Applications.”

And, finally, a long-overdue clarification: Last summer, when Berkshire began trimming back its position in BYD, I tried to be very careful to distinguish that each new filing related only to the Hong Kong-listed shares of the EV maker. Somewhere along the way, though, I stopped doing that and confused myself and (probably) others in the process. So, when I wrote that Berkshire still owns over 8% of BYD, that’s not entirely accurate. Berkshire owns that amount of BYD’s Hong Kong-listed shares — not 8-ish% of the company overall. (BYD is also listed on the Shenzhen Stock Exchange in China.) According to my back-of-the-napkin math, Berkshire currently owns approximately 3.2-3.3% of BYD as a whole.

This isn’t my first dumb mistake — and it certainly won’t be my last. When in doubt, please remember that I’m an idiot.

A Closer Look at Berkshire Hathaway’s 50th Anniversary Book

I’m very glad that so many people are enjoying Tuesday’s article: Warren Buffett’s 1969 Annual Letter — Yes, It Actually Exists.

In it, I discovered that Buffett’s final annual partnership letter — written shortly before BPL closed down — has been hiding in plain sight all along in Celebrating 50 Years of a Profitable Partnership, a book released for Berkshire Hathaway’s 50th anniversary in 2015 and still available for sale, today, on the company’s website.

The entire thing is a treasure trove of Berkshire history with many never-before-seen artifacts and documents — including an extensive history of Berkshire’s pre-Buffett textile operations and BPL’s subsequent takeover in 1965. Plus, observations from Buffett himself are sprinkled throughout the book. (I found his continued disdain for Seabury Stanton to be particularly amusing. Buffett doesn’t give up on a grudge easily!)

To be fair, I don’t think anyone liked Seabury very much. His own brother, Otis, played a pivotal role in selling control of Berkshire to Buffett’s partnership.

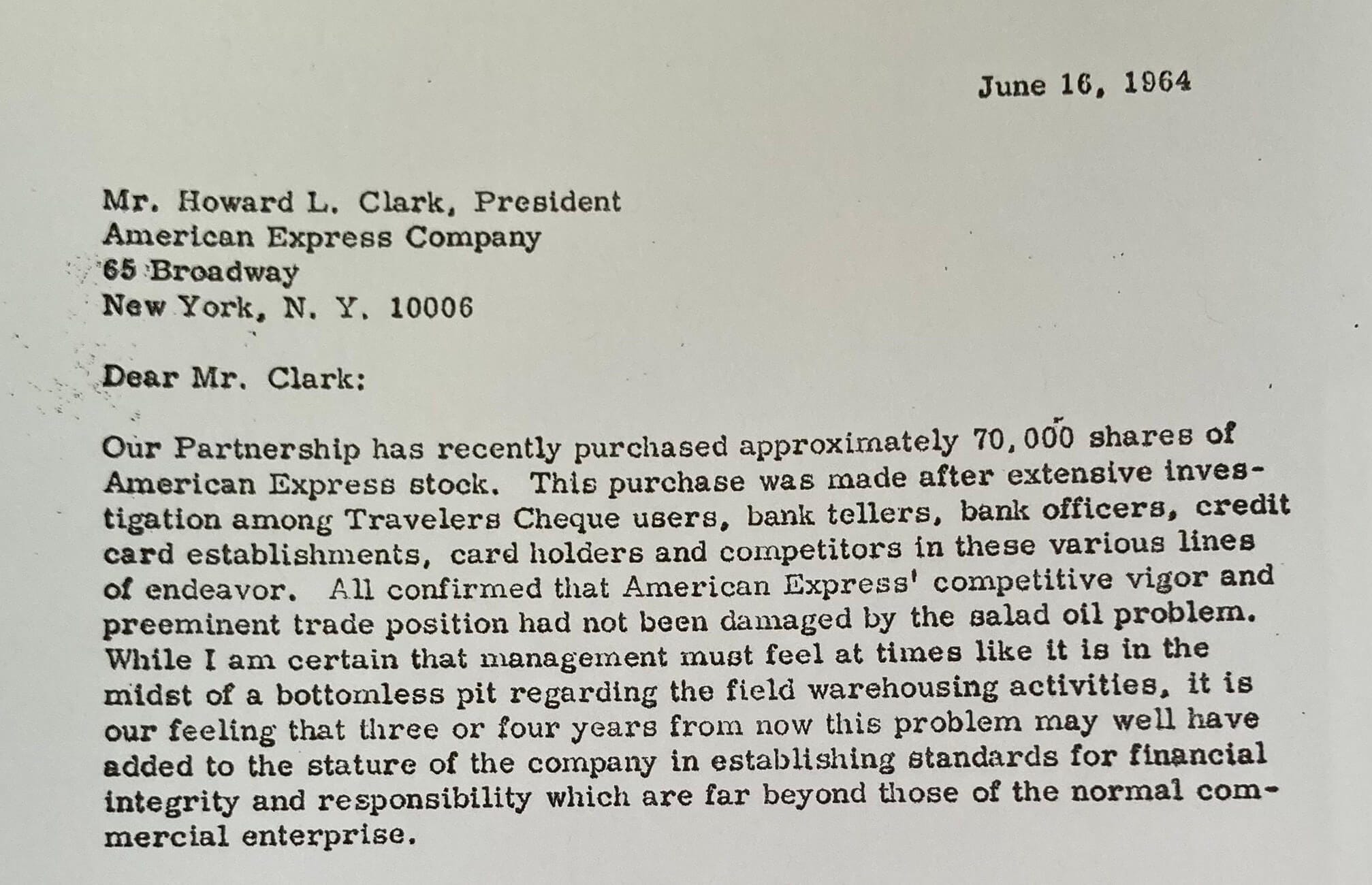

Another highlight is the correspondence between Buffett and American Express during the so-called Salad Oil Scandal in 1964. What can I say, I’m a sucker for old Buffett letters. Especially ones that explain his reasons for buying a particular stock.

In Buffett parlance, the 50th anniversary book’s intrinsic value is way higher than its $25 sticker price. An essential addition to any Berkshire fan’s library.

More Must-Reads

Other awesome things that I read this week…

Fewer Losers, or More Winners? (Howard Marks)

“There’s such a thing as the risk of taking too little risk. Most people understand this intellectually, but human nature makes it hard for many to accept the idea that the willingness to live with some losses is an essential ingredient in investment success.”

Six Rules for Financial News Tom Morgan

“It’s pretty obvious that human behavior is one of the most predictable and enduring aspects of financial markets. It’s perhaps less obvious that case studies are generally more useful than lists of biases or rules … This means some of the most valuable financial content you can read is historical stories that illustrate recurring patterns of human behavior.”

Valuation (Dividend Growth Investor)

“Valuation is taking into consideration both ‘value’ and ‘growth’ schools of thought, without looking at things in isolation. Per Warren Buffett, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive.”

Negative Lollapalooza Effects The Rational Walk

“Investing can be a solitary endeavor. The best opportunities are, almost by definition, the ones that the rest of the market has overlooked. Irrational pessimism and short-term thinking have the power to cause market prices to detach from any reasonable assessment of intrinsic value. When this occurs, the intelligent investor has to be willing to act quickly and forcefully to take advantage of the opportunity. In other words, it is important to discard the notion of requiring social proof prior to acting on an investment opportunity.”

Ben Graham to Warren Buffett: The Postcard That Taught Me How To Value A Child (Beyond Ben Graham)

“What can we learn from Ben Graham’s postcard to Warren Buffett? That no one needs to be perfect.”

"This isn’t my first dumb mistake — and it certainly won’t be my last. When in doubt, please remember that I’m an idiot." 🤣🤣🤣 Endeavor to do meaningful things, and mistakes are inevitable. 🙏