20 Thoughts on Berkshire Hathaway's Q3 2023 Performance

Lots to unpack in Berkshire's latest quarterly report...

Happy Monday and welcome to our new subscribers!

Special thanks, too, to those who recently became paid supporters! ❤️

Leading up to Berkshire Hathaway’s Q3 2023 earnings report on Saturday morning, most analysts predicted a sizable boost in operating earnings for the conglomerate. I even saw a few that expected a 20-30% gain from Berkshire’s owned businesses.

But, as it turns out, Berkshire’s third quarter results were even better than that.

You might not know it from some of the media headlines over the weekend — which, predictably, focused on the $12.8 billion net loss caused by falling stock prices — but I think we’re all used to that particular quirk by now.

Well, without further ado, on to the main event…

(1) Warren Buffett and Charlie Munger have long recommended that shareholders look first to operating earnings when evaluating Berkshire Hathaway’s performance. This shows the results of the conglomerate’s many owned businesses, which often get shoved out of the spotlight by a misleading net income number. And we have mark-to-market accounting to thank for that. Much more on that down below.

In Q3 2023, Berkshire’s operating earnings soared by 40.6% — while the company reported a bottom line “loss” of $12.8 billion.

(2) Accounting should illuminate — not complicate. For companies like Berkshire Hathaway, the mandate to include unrealized gains or losses in net income will almost always lead to confused analysis and distorted results.

I don’t care about misleading headlines (“Berkshire Loses Money!”) for Warren Buffett or Charlie Munger’s sakes. Both men are strong enough to withstand the slings and arrows. But I fear that this muddled reporting might confuse individual investors who don’t obsessively hang on every last piece of public information about Berkshire.

It would be terribly unfortunate if this accounting quirk caused anyone to get the wrong idea about the company’s actual performance and decide to sell off what should be a cornerstone of their portfolio. All because of temporary, unrealized, paper losses.

(3) Of course, no one knows this better than Berkshire Hathaway. In an accompanying press release, CFO Marc Hamburg wrote in bold: “The amount of investment gains/losses in any given quarter is usually meaningless and delivers figures for net earnings (losses) per share that can be extremely misleading to investors who have little or no knowledge of accounting rules.”

And, in his latest annual letter, Warren Buffett chided the “acrobatic behavior” of GAAP-mandated earnings, which “fluctuate wildly and capriciously at every reporting date”. He continued: “Their quarter-by-quarter gyrations, regularly and mindlessly headlined by media, totally misinform investors.”

Amen.

(4) Back in August, I wrote: “In Q2 2023, Apple was jet fuel for Berkshire Hathaway’s rocketing bottom line. But, in the future, it could just as easily become a massive anchor weighing down the company’s results … All without selling a single share.” And that’s exactly what happened in the third quarter. Apple, with its outsized place in Berkshire’s stock portfolio, fell by 11.7%.

Other major holdings like Bank of America, Coca-Cola, and American Express also sank in price during the quarter. Warren Buffett did not sell and lock in any of these losses. They exist only on paper. Yet they’re the biggest drivers behind Berkshire’s $12.8 billion “loss” in the quarter. Make it make sense.

(5) Before anyone jumps on me, I’m not saying that the values of Berkshire Hathaway’s stock holdings don’t matter. Of course, they do. But, owing to the portfolio’s immense size, even modest quarter-to-quarter price changes can lead to crazy swings in net earnings. This only reinforces the worst impulses of investors — focusing their attention on short-term price movements instead of long-term value.

It empowers the voting machine aspect of the market at the expense of the weighing machine. And that’s the last thing any of us should want.

(6) Berkshire Hathaway’s 40.6% increase in operating earnings was fueled by the remarkable performance of its insurance segment. Underwriting turned a $2.4 billion profit, led by “relatively low catastrophe losses” so far in 2023. (Fingers crossed that they stay that way. Florida’s hurricane season is almost over!)

For example, Berkshire suffered $3.9 billion in losses from significant catastrophe events in 2022 (mainly via Hurricane Ian) — but that has dropped to just $590 million through the first nine months of this year.

(7) Warren Buffett continued to park Berkshire Hathaway’s massive cash pile in short-term Treasury bills — and that provided a huge boost to insurance results. Thanks to rising interest rates, Berkshire made $1.7 billion of investment income from these short-term treasuries during the third quarter. That’s good for a 330.7% increase from a year ago.

(8) GEICO scored a $1.05 billion pre-tax underwriting profit in Q3, making it three profitable quarters in a row after six straight in the red. The auto insurer’s current plan is simple: trade growth for profitability. And it’s working.

In 2023, GEICO has slashed advertising expenses and, as a result, now holds 2.3 million less policies-in-force than before. But, over that same period, average premiums per auto policy are up 16.8%. This strategy probably won’t work forever, but it seems to have put GEICO back on the right track after a brutal couple of years.

Congrats to Todd Combs — pressed into double duty here — for leading the insurer out of the wilderness and back to consistent profitability!

(9) GEICO posted a very impressive 89.3% combined ratio in the third quarter. Happily, its full-year performance is shaping up to be much better than vice chairman Ajit Jain predicted back at the annual meeting in May, when he guessed that GEICO’s combined ratio would end up “just south of 100%” in 2023. Barring an utter disaster in the fourth quarter, GEICO should finish up the year well below that number.

Berkshire Hathaway Primary Group (88.5%) and Berkshire Hathaway Reinsurance Group (74.1%) also achieved excellent combined ratios in the quarter. Berkshire’s insurance operations are riding pretty high these days.

(10) Berkshire Hathaway’s cash pile ballooned up to $151.9 billion. And, while some people angst over Warren Buffett and Charlie Munger holding so much cash, I rest comfortably knowing that they have so much dry powder with which to attack the market. I’d rather Buffett and Munger remain patient and carefully pick out just the right pitch to swing at — because that inevitably means good things for shareholders.

FYI: I don’t typically include cash from “Railroads, Utilities, & Energy” in this total, so you may see a bigger cash number — like $157 billion — elsewhere. Berkshire Hathaway Energy, BNSF, etc. need that cash for their own operations.

(11) Speaking of big numbers, Berkshire Hathaway’s insurance float now clocks in at $167 billion. The asynchronous nature of insurance — a company receives premiums from customers, but doesn’t pay out anything until claims come due — creates what is known as “float”. This collect-now, pay-later business model leaves insurers holding large sums of money that can be invested to create a new avenue of profitability.

Even better, if the insurer’s underwriting breaks even, this float is basically free. The company pays nothing for access to lots of investable money. That’s exactly what happened in the third quarter with Berkshire’s $2.4 billion underwriting profit.

Just imagine showing up at a bank and asking to borrow $167 billion at a 0% interest rate. You’d probably get laughed out of the building. But that’s kind of what Berkshire’s insurance operations have managed to achieve. If there’s a secret to Warren Buffett’s success, that’s it right there. He expertly builds up float and then uses it to drive greater and greater returns for Berkshire. Long may that continue.

(12) We won’t get a full picture of Berkshire Hathaway’s Q3 2023 investing activity until its 13F comes out next week, but it appears that Chevron (once again) ended up on the chopping block. If my back-of-the-napkin math is correct, Warren Buffett sold between 10-11% of his CVX 0.00%↑ position during the third quarter.

The Oracle has now pared back on Chevron in four consecutive quarters, but it still remains one of Berkshire’s largest stock holdings. Much more on this coming next week in my 13F wrap-up.

Become a paid supporter today and receive immediate access to four annotated transcripts full of wit and wisdom from the top names at Berkshire Hathaway.

Paid subscribers will also continue to receive a new annotated transcript each month.

(13) BNSF’s earnings fell by 15%, which comes hot on the heels of a 24% drop in Q2. These are tough times on the rails. Freight volumes dipped 5% in the third quarter — with consumer products and coal the two biggest culprits.

The railroad’s operating ratio increased to 68.4% in Q3. For comparison, the Union Pacific reported a 63.4% operating ratio during the same period. (Lower is better.)

(14) Berkshire Hathaway Energy suffered an earnings decline of 69%. This eye-catching result mostly stems from mounting litigation against PacifiCorp relating to the deadly wildfires in California and Oregon during 2020 and 2022. The BHE subsidiary increased its liability for estimated probable wildfire losses by $1.4 billion this quarter, which really put a crimp in this segment’s results.

And, worryingly, this might not be the end of the story. Berkshire’s 10-Q: “It is reasonably possible PacifiCorp will incur significant additional Wildfire losses beyond the amounts currently accrued.”

(15) Unfortunately, another BHE subsidiary faces its own legal problems. Just this past week, a jury returned a $1.8 billion verdict against real estate brokerages — including HomeServices of America — over allegedly inflated commissions.

HomeServices pledges to “vigorously appeal on multiple grounds the jury’s finding and damage award” — so this one might take a while to play out. Stay tuned.

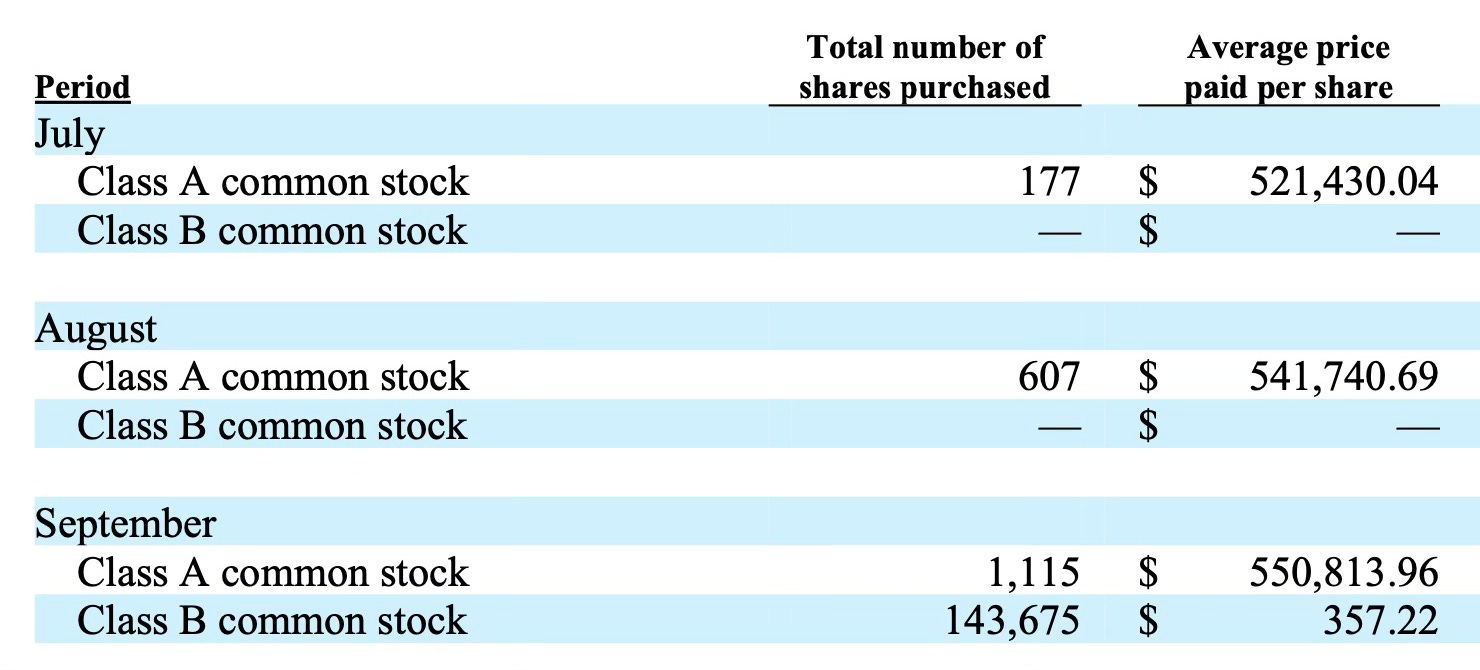

(16) Warren Buffett spent $1.1 billion on stock repurchases during the third quarter. That’s the lowest quarterly total of 2023 to date — with $4.4 billion in Q1 and $1.3 billion in Q2. Interestingly, Buffett was particularly active in this arena in September, when prices of both Class A and Class B shares were higher than they are right now.

Berkshire Hathaway only executes buybacks when Buffett and Munger “believe that the repurchase price is below Berkshire’s intrinsic value, conservatively determined”. So, by definition, two of the greatest investors of all time feel that Berkshire is undervalued at current prices. Do with that what you will.

(17) Here’s what Warren Buffett spent each month on share repurchases:

July — $92.3 million

August — $328.8 million

September — $665.5 million

(18) Warren Buffett ramped up the buybacks even more in October. Based on the updated share count that appears on the first page of Berkshire Hathaway’s 10-Q, he repurchased approximately 1,544 more Class A equivalents between October 1-24.

Safe to assume that Buffett spent more in October on buybacks than he did in any single month of the third quarter.

(19) Berkshire Hathaway’s MSR (Manufacturing, Service, & Retailing) segment inched up by 2.9% in Q3. I’ll probably dig into these numbers a little more in Friday’s issue of The Berkshire Beat, but I’m very happy to see Precision Castparts post another strong quarter. PCC’s pre-tax earnings shot up 43.1% due to an increase in sales and improved efficiencies.

(20) Jazwares — and its $847 million of revenue so far in 2023 — once again received a shoutout in this quarterly report. A true hidden gem of the Alleghany acquisition.

And if Jazwares ever wants to sponsor an issue of this newsletter, I will accept payment in Warren Buffett and Charlie Munger Squishmallows.

Just a peep about GEICO layoffs of approximately 6% of it's workforce. That's how they leverage their expenses in the insurance sector.