Warren Buffett's Tried & True Inflation Hedge, Learning to ❤️ Falling Stock Prices, and the Nine Lives of Big Tobacco

At times like this, people should be knocking down the door of Mr. Market’s house like it’s Black Friday at Walmart. Instead, they avoid the place like the plague.

Happy Monday!

GRD dropping some knowledge to start off the week:

Can’t Stop, Won’t Stop: Berkshire Adds More Oxy 🛢

Back in 1956, Warren Buffett sang (or, in this case, wrote) the praises of Oil & Gas Property Management as “The Security I Like Best” in the pages of The Commercial and Financial Chronicle.

A more fitting title for my selection would be “The Inflation Hedge I Like Best”. Should inflation continue, O & G may well be the vehicle to give the investor the same super-charged performance that highly leveraged investment trusts and warrants did in the early ‘40s.

In 2022, inflation is back with a vengeance — and, once more, Buffett seems to have tabbed oil/energy as his inflation hedge of choice.

Last week, Berkshire Hathaway bought 9.6 million more shares of Occidental Petroleum, boosting the company’s total stake to 16.3% of the Texas oiler. That makes Berkshire, by far, Oxy’s largest shareholder.

And, when you factor in the preferred stock and warrants from the Anadarko loan, Berkshire actually “owns” around one-third of Oxy as a whole.

That has set tongues wagging about whether or not Buffett might ultimately want to purchase Occidental Petroleum outright.

Neal Dingmann of Truist Securities:

We believe there is a good chance billionaire investor Warren Buffett buys the remaining two-thirds of shares of Occidental Petroleum that he and Berkshire Hathaway do not own once the company becomes investment grade.

Oxy, as a whole, won’t come cheap. Buffett would have to shell out close to $60 billion more to close this deal.

Individual shares, though, continue to trade at surprisingly low prices. Oxy boasts a forward P/E of just 7 — a bizarrely low valuation for a stock already up 85% in 2022.

But its share price did drop close to 20% in June, which likely enticed Buffett and co. to scoop up a few million more shares.

In addition to the growing stake in Occidental Petroleum, Buffett also boosted Chevron into Berkshire’s fourth-largest portfolio holding.

Rising oil prices allow the Chevrons and Occidental Petroleums of the world to get right after a brutal few years. In April 2020, crude oil contracts dropped into negative territory, which (along with other Covid stuff) wreaked havoc on Big Oil’s balance sheets.

The top companies all took on lots of debt in order to survive, casting some doubt on their future prospects, but the many odd events of 2022 have come to their rescue. Strong profits (and free cash flows) mean that the oil giants can clear their decks of recently-incurred debt, fund new acquisitions and projects (including renewables), and return money to shareholders.

No surprise that Buffett likes what he sees here.

Learn to Love Falling Stock Prices ❤️📉

As the great Genevieve Roch-Decter says, “The stock market is the only place that goes on sale and everyone’s sad.”

This idiosyncrasy of the investment community — some also liken it to cognitive dissonance — doesn’t make a whole lot of sense.

Who wouldn’t want to buy pieces of top-notch companies at low, low prices?

At times like this, people should be knocking down the door of Mr. Market’s house like it’s Black Friday at Walmart. Instead, they avoid the place like the plague.

Much like me, John Huber of Saber Capital Management enjoys re-reading Warren Buffett’s annual letters and transcripts of his Q&As to wrest out every last bit of wisdom. (Judging by our respective net worths, John is much better at this than me.)

And, from Buffett’s 1997 letter, he took away three lessons that seem especially applicable to today’s bear market:

(1) If you’re a net buyer of hamburgers, you want a lower price of burgers. If you’re a net buyer of gas, you want lower gas prices. If you’re a net buyer of stocks, you should want lower stock prices. It really is that simple, and the fact that this mindset is so foreign to most investors is what gives those with the right mindset a big advantage.

The mental tension of rooting for lower stock prices, although that means your current positions will likely (temporarily) drop in nominal value, remains a constant battle for the intelligent investor.

Remember: You should be as excited as those manic Black Friday shoppers.

(Without all of the trampling, though.)

(2) Companies that are buying back shares are the corporate equivalent of net savers. They earn more than they spend and thus benefit from a lower stock price as each dollar spent on buybacks acquires more value with a lower share price, benefiting the long-term owners of the company.

Along the same lines, companies are better served repurchasing shares when prices are low, too. We’ve all seen countless examples of cash-rich companies announcing lavish buyback plans — even though their share prices were touching all-time highs.

Then, when times get tough (and prices drop), those same companies pare back on the repurchases. Just when it would make the biggest impact.

Needless to say, that’s a very inefficient use of money.

(3) To the extent that lower stock prices coincide with difficult economic conditions, the best companies often benefit indirectly from lower share prices as they are able to take market share, thus improving the long-term earning power of the company (and, ultimately, the long-term share price).

If you’ve built a portfolio full of strong blue-chips, economic downturns often fuel big gains in market share and profits.

That might sound a little weird, so let me explain. Every industry is full of smaller (and, in some cases, bigger) competitors swimming naked when the tide goes out. While those blushing beachgoers are ruined, the surviving well-capitalized businesses feast on the remains and grow ever larger.

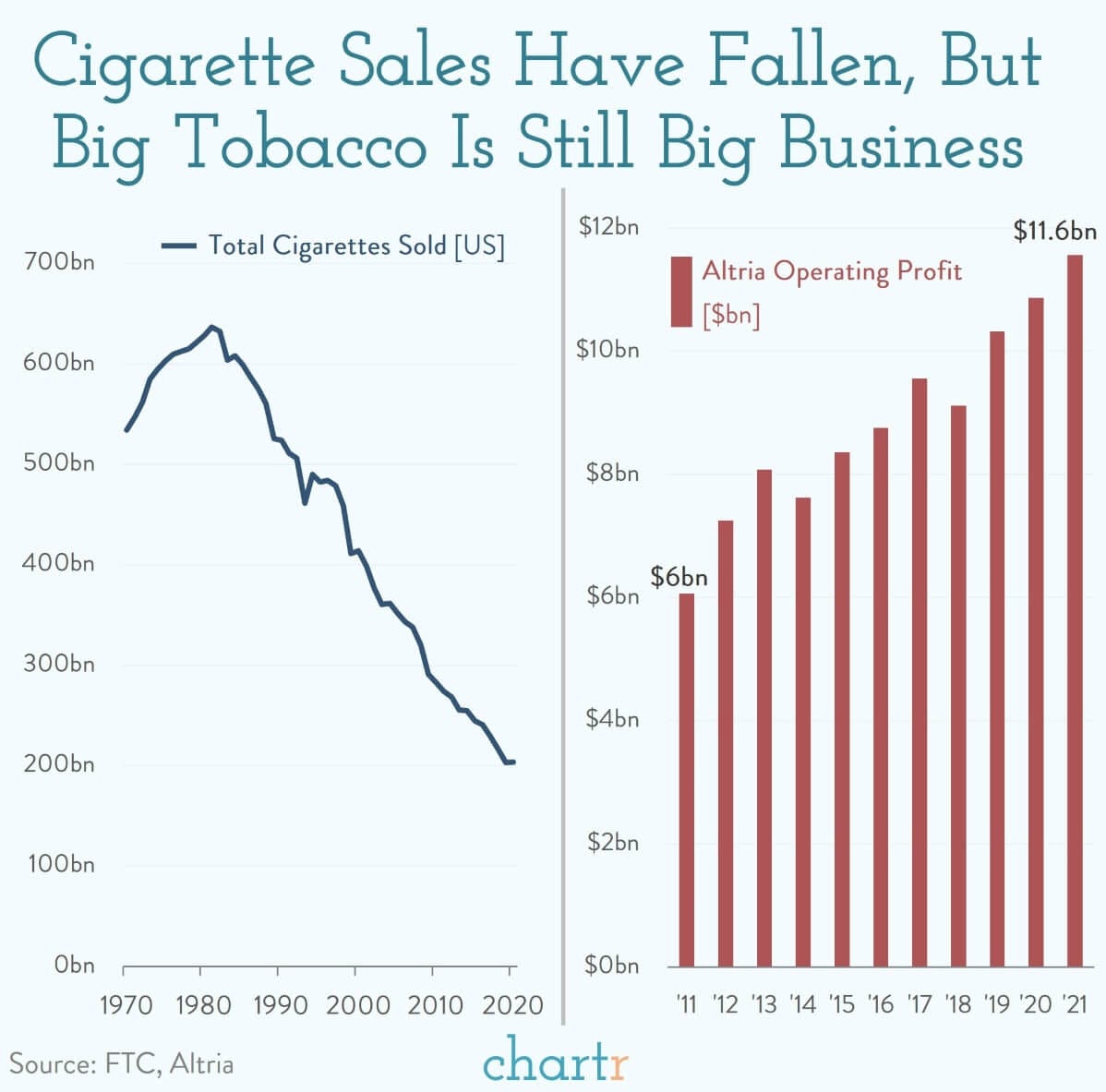

🚬 The Nine Lives of Big Tobacco

Last week, the FDA banned vaping pioneer Juul from selling its products in the United States. That decision was immediately stayed pending appeal, meaning that Juul users will get to enjoy their e-cig of choice for a few more months (or years).

Big blow for Altria, which bought 35% of Juul for $12.8 billion in 2018. Since then, though, Altria has written down the value of this investment several times — and now faces the sad prospect of a total loss if the FDA’s decision stands.

But anyone counting Altria — or other members of Big Tobacco — out need to brush up on their history. These companies have managed to survive (and, in some cases, thrive) in the face of unrelenting governmental and societal regulation. They’ve managed to shrug off plummeting cigarette sales, advertising bans, warning labels affixed to packaging, slick no-smoking ad campaigns, and more.

And, despite all that, tobacco companies are more profitable than ever.

How is that possible?

In short, the tobacco kings raise prices on cigarettes faster than people stop smoking. Altria, Philip Morris, British American Tobacco, Imperial Brands, et al. can flex some serious pricing power whenever the need (or mood) arises.

And, while government regulations significantly slowed cigarette sales, they’ve done very little to Big Tobacco’s bottom line. In fact, they’ve probably helped.

When the U.S. outlawed cigarette advertising on television and radio in the 1970s, that forever entrenched the existing companies as the only players in the game. Companies in basically every other industry must jealously guard their market share, pouring money into R&D and advertising to keep their products and brand names in front of customers’ eyes.

Not so for the tobacconists, who have Scrooge McDuck-like money bins full of profits and few corresponding expenses. They can afford to pay sizable dividends, repurchase shares (usually at low prices because ESG funds won’t touch ‘em), and perhaps even invest the rest in diverse fields.

(For example: (1) Philip Morris used to own Kraft, and (2) Altria currently holds a 10% stake in Anheuser-Busch.)

Sitting atop an industry that’s basically a government-enforced monopoly is a pretty sweet deal.

If you’ve enjoyed reading this issue of Kingswell, please hit the ❤️ below and share it with your friends so they don’t miss out. It costs you a total of $0 and means the world to me. Thank you!

Disclosure: This is not financial advice. I am not a financial advisor. Do your own research before making any investment decisions.