Walter J. Schloss: An Investor for All Seasons

In 1989, Schloss spoke with OID about his long career on Wall Street and how the Grahamian approach to spotting undervalued stocks never truly goes out of style

Happy Tuesday and welcome to our new subscribers!

Of all Benjamin Graham’s many acolytes, one in particular stuck to his mentor’s methods more than most. Walter J. Schloss learned his trade at the Graham-Newman investment firm (even sharing an office with Warren Buffett at one point), before striking out on his own in 1955.

Schloss, like Graham, played a completely different game than most of his contemporaries. He hunted for “cigar butt” stocks, named for their resemblance to discarded cigar butts that nevertheless still had one last puff of smoke in them. These could often be had at rock-bottom prices, with Schloss hoping to catch any run-up in price before flipping them for a profit.

Buffett started out in the same style, but eventually transitioned to buying excellent companies at fair prices with a preferred holding period of forever.

Schloss, though, never budged.

He excelled at this purely quantitative game of arbitrage — with little to no concern over the quality of a given company — and unloaded his positions as soon as the price imbalance corrected itself.

And it worked.

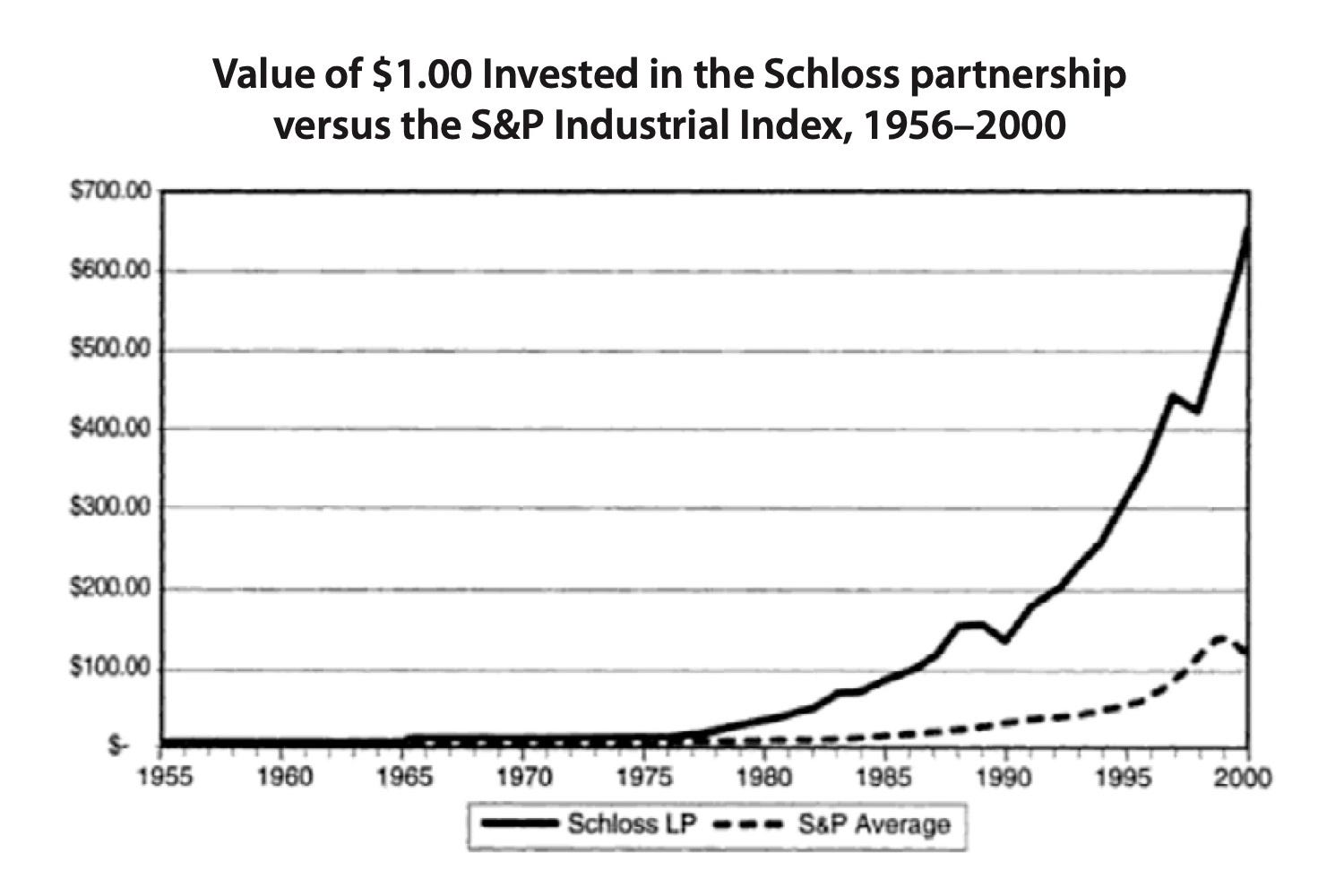

During five decades running Walter J. Schloss & Associates (later re-named Walter & Edwin Schloss Associates after his son joined), he achieved 16% compounded annual returns — after fees — for his partners. And he did it all without a computer, choosing to analyze newspapers and Value Line reports instead.

In 1989, Walter (alongside his son, Edwin) spoke with Outstanding Investor Digest about his long career on Wall Street and how the Grahamian approach to spotting undervalued investment opportunities never truly goes out of style.

Here is what I learned…

Be Patient

Even Walter Schloss, who ran his investment kingdom with no computer and just a single telephone, could get a little too amped up when opportunity came knocking.

When OID asked about the most common mistake made at Walter & Edwin Schloss Associates, Schloss the Younger answered:

Being too aggressive initially. Buying so much of a stock initially that, when the price moved lower, it took too much capital to average down. We’ve occasionally bought so much that we couldn’t buy as much as we’d like when it went down further without becoming overly concentrated.

We all know that rush of excitement when a stock that we’ve followed and researched and analyzed and daydreamed about owning finally drops into the buy zone.

The temptation to splurge all of your allotted funds on this position at once — in fear that the price might suddenly soar if you don’t jump in with both feet RIGHT NOW — is a mighty strong one. (Believe me, I know.)

Most investors can’t get the money out of their pockets fast enough.

A patient build-up, though, almost always turns out better. Sure, the price might run away from you before your position reaches its optimal size, but that’s no reason to discard your emotional discipline and take rash action.

How often do you truly buy at the bottom? At least in my experience, the answer is never. So why spend all of your money in one go at the very start — especially when you’ll likely get the chance to add more shares (at cheaper prices) in the near future?

No one ever said that it’s easy to remain patient while playing the money game, but that tends to be the surest path to life-changing wealth.

Know Thyself

Walter Schloss once said, “We would have done better if we just had bought Berkshire Hathaway stock and held on.”

His son agreed — but pointed out, “We wouldn’t have had so much fun!”

Schloss liked to stay active in the market. He felt that it kept him engaged. So he built a big portfolio (which he likened to Noah’s Ark — two of everything) and kept stocks moving in and out.

Edwin and I like the idea of having a little action. That may not be good from a logical point of view, but it’s good from an emotional point of view.

If we owned the same five companies for the next ten years because we believed in the businesses and all we did was sit here and look at each other, it would be no fun. It may be a profitable way of investing, but you have to have some fun in what you do.

Of course, the types of companies that Schloss bought lent themselves to this approach.

It’s extremely risky to hold cigar butt stocks for too long. Schloss was only trying to catch the price swing up from an undervalued starting point — and then he cashed out. If he missed that window of opportunity, the whole investment could go up in smoke.

This exact style isn’t necessarily something to emulate — especially for an inveterate buy-and-hold investor like myself — but we can all learn from the way that Schloss built his system to accommodate his own unique emotional/personal quirks.

Speaking for myself, I would love to own the same five stocks for decades. That’s not boring to me. But Walter Schloss understood himself well enough to know that that wouldn’t work for him. So he structured his investing strategy in a way that did.

The only good plan is the one that you will be able to stick with.

Know thyself — and invest accordingly.

Have the Courage of Your Convictions

When Walter Schloss decided to leave Graham-Newman in 1955 and hang his own shingle, two of the most important people in his life were against it.

[My mother] begged me not to go into business for myself.

I didn’t have the money, but I had an opportunity. Someone said they’d put some money into my partnership.

Mother pointed out that I had two small children and shouldn’t take the risk. Well, we are both pleased that she was completely wrong.

Ben Graham, meanwhile, feared that the market was too high in 1955 — and that this was not the ideal time for his young protege to strike out on his own.

I admired Graham tremendously — and I was going into the business at just the time when he was saying the market was too high.

It was just one of those things. You do what opportunity allows you to do. It turned out to be a fabulous decision. I didn’t know it at the time.

You really have to stick to your guns no matter what other people think.

Schloss could not be dissuaded from starting his own investment firm — and then spent the next five decades making both himself and his partners very rich.

I think he made the right call.

Loose Lips Sink Ships

Much like Warren Buffett did with Buffett Partnership Ltd. in the 1950s and 1960s, Walter Schloss kept his investment holdings a closely-guarded secret.

In both cases, the men were purchasing scarcely-traded, somewhat inactive securities that could become impossible to buy if others got in on the bidding. Allowing coat-tailing copycats to know what you were buying (or selling) needed to be avoided at all costs.

But not just that — many investors would grumble if they knew about the collection of mediocrities (at least from a company quality standpoint) that made up a cigar butt investor’s portfolio.

As Schloss told OID:

One of our partners said, “Walter, I have a lot of money with you. I’m very nervous about what you own.”

So I made an exception and said, “I’ll tell you a few things that we own.” I mentioned the bankrupt rail bonds and a couple of other things we owned.

He said, “I can’t stand knowing that you own those kinds of stocks. I have to withdraw from the partnership.”

He died about a year later. That’s one of the reasons we don’t like to give people specifics.

What makes that story even sadder is that Schloss mostly limited his partners to those who actually needed his help. Not millionaires looking to squeeze out an extra zero or two on their net worth, but hard-working individuals trying to grow their nest egg.

Schloss figured that secrecy was the best way to protect his partners from themselves.

All of this added up to make Walter Schloss one of the best investors of all time.

And one friend, in particular, never missed a chance to sing his praises.

On February 3, 1976, Warren Buffett wrote to his “Hilton Head Group” of fellow investors about the incredible market performance of Schloss’s firm.

You may remember that I went to work for Graham-Newman in 1954. Walter left in 1955. And then Graham-Newman closed up in 1956. I would prefer not to dwell on the implications of this sequence.

In any event, armed only with a monthly stock guide, a sophisticated style acquired largely from association with me, a sub-lease on a portion of a closet at Tweedy, Browne and a group of partners whose names were straight from a roll call at Ellis Island, Walter strode forth to do battle with the S&P.

Walter has had five down years compared to seven for the S&P. His superiority in such down years would indicate that not only is he a man for all seasons, but that he has a special strength when facing a head wind.

Why did Buffett enthusiastically call Schloss a “man for all seasons”?

During the economic doldrums of 1974, Schloss crushed the S&P 500 by more than 20%. Then, in a high-flying market the following year, he once again beat the benchmark 52.2% to 36.9%.

In 1994, Buffett wrote another letter:

Walter continues to outperform managers who work in temples filled with paintings, staff and computers. And he accomplishes this feat by rummaging among the cigar butts on the floor of capitalism: It’s quite a 38-year record, a tribute to Ben [Graham] as a teacher, Walter as a student, and to the advantage of a free puff.

At the bottom of the letter, Buffett wrote by hand:

Walter,

Please put me in the partnership — retroactively to 1955.

But Walter J. Schloss saved his best for last.

At the height of the dot-com bubble, he shorted both Amazon and Yahoo — allowing his fund to outpace the S&P 500 by 37% in 2000 and 24% in 2001.

What a legend.

If you’ve enjoyed reading this issue of Kingswell, please hit the ❤️ below and share it with your friends (and enemies) so they don’t miss out. It only costs you a few clicks of the mouse, but means the world to me. Thank you!

Disclosure: This is not financial advice. I am not a financial advisor. Do your own research before making any investment decisions.

Awesome read and tribute! Many Thanks!

Great read, Kevin. Thanks.