The Berkshire Beat: May 1, 2026

All of the latest Warren Buffett and Berkshire Hathaway news!

(1) Each spring, a caravan of the faithful — tens of thousands of Berkshire Hathaway shareholders from every corner of the globe — makes a pilgrimage to Omaha for the conglomerate’s annual meeting. For decades, that meant one thing: Warren Buffett and Charlie Munger holding court, fielding questions on everything from markets and mortality to philosophy and peanut brittle. An era unto itself.

But, tomorrow, a new one begins.

Greg Abel takes center stage as CEO for the first time — and a few new faces will join him up on the dais throughout the day. Abel will deliver a general business update at 9:30 a.m. ET, before opening the floor to questions alongside vice chairman Ajit Jain.

After lunch, he will return with BNSF Railway CEO Katie Farmer and Berkshire’s new President of Consumer Products, Service and Retailing (plus NetJets CEO) Adam Johnson in tow for the afternoon Q&A session. Watch the whole thing here.

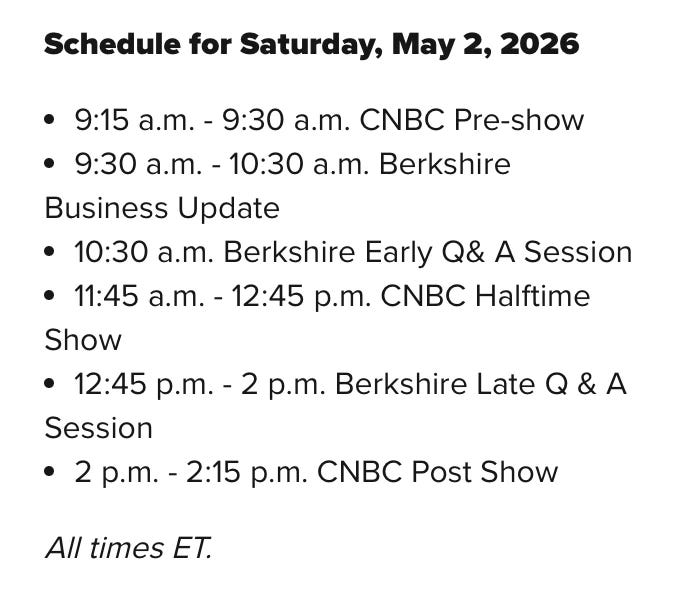

The full schedule for tomorrow’s proceedings:

And, don’t forget, the fun really kicks off at 8 a.m. ET when Berkshire releases its Q1 2026 earnings report. A little light reading to whet our appetites for the main event.

(2) Will as many people still show up for a Buffett-less meeting?

Early signs say yes. Berkshire told CNBC last week that credential requests are tracking closely with previous years — running slightly behind 2024 and 2025, but ahead of 2023. Perhaps that’s an indication that Berkshire as an institution is bigger than any one person. Even when that person happens to be Warren Buffett.

It helps, of course, that not everyone making the trip to Omaha is chasing investment wisdom. Berkshire noted that Nebraska residents make up about 60% of attendees — with many coming as much for the shareholder discounts at NFM and Borsheims as anything else. Berkshire is, at heart, a collection of businesses that people genuinely love. That’s one thing that hopefully never changes — no matter who is CEO.

(3) Chris Bloomstran of Semper Augustus — whose annual client letters are essential Berkshire reading — sat down with The Investor’s Podcast ahead of this weekend’s meeting. The wide-ranging discussion touched on his own intrinsic value estimate for Berkshire, the conglomerate’s recent performance, and how fresh capital flooding into insurance markets will likely give Ajit Jain and co. pause.

Regarding the meeting itself, Bloomstran predicts something of a tonal shift from the Buffett and Munger era. “I expect this [AGM] to be a heck of a lot more business focused,” he said. “It’s going to be shorter, but hearing from these folks running the subsidiaries about what’s going on and what concerns them is going to be great.”

Basically: Fewer life lessons, more operational detail.

(4) Bloomstran also laid out his own framework for evaluating Greg Abel. It hearkens back to something Charlie Munger used to say — that when you get a trip to the pie counter, you best load up your plate. You won’t get many chances, after all.

“I’m going to judge Greg by how hard he leans into opportunity when it comes,” he said, “and it’s [probably] only going to come in a crisis or a recession.”

That’s when Abel must prove his mettle — even though such opportunities are often more palatable in hindsight than in the heat of the moment.

“It’s not easy when you’re staring down the barrel of a financial crisis,” said Bloomstran. “It’s not that easy to pull the trigger.”

(5) The second edition of The Complete Financial History of Berkshire Hathaway hit bookstores earlier this week. The original chronicled Berkshire’s journey up through 2019 — a rigorous, year-by-year accounting of how Buffett and Munger built one of the most consequential businesses in American history.

But, in light of Buffett’s retirement, author Adam Mead knew an update was in order.

This new edition completes the arc of Buffett’s tenure atop the conglomerate, capturing the final chapters of his legendary capital allocation record.

I caught up with Adam to find out more about the new material and why this book deserves a spot on every serious investor’s bookshelf.

Q: Can you run through some key points that you added to the second edition?

Mead: Apple became 50% of the investment portfolio before being sold down to a still-large 25% of the portfolio and giving Berkshire a $90 billion gain in 2024 alone.

Alleghany is interesting. When you think about how large it is by itself — its insurance operation, multiple non-insurance businesses — and yet it amounted to just 2.4% of Berkshire’s equity capital. Said another way, it consumed just three months of Berkshire’s cash generation. Incredible!

The Japanese investments were a masterstroke of simply searching the world for opportunity and acting on it. Not only that, but financing it with 1% yen-denominated bonds that also mitigated currency risk.

Pilot was a fascinating story that brought rare intrigue into the halls of Berkshire Hathaway. I enjoyed writing about Pilot not only because of the story but because of the details that came out because of it. The lawsuit specifically stated the valuation metric Berkshire used [in the acquisition].

I think Alleghany demonstrates the challenge moving forward. The figures have become so large. Berkshire will need big acquisitions. But it can also make a lot of progress on other fronts. Berkshire repurchased $72 billion worth of its own shares between 2020 and 2024. That will move the needle over time!

Q: You have studied Berkshire’s history in painstaking detail. What did you learn about the business that you couldn’t have gotten any other way?

Mead: In a relatively short 825 pages — I said relatively — you can view the entire history of Berkshire. I learned things from my own writing about Berkshire during the editing process, where I went back and read longer sections all at once.

Two things stand out — what doesn’t change and what does.

What doesn’t change is the basic strategy of doing the best with what’s in front of you at any given time, given the opportunity set, and applying what Munger called basic horse sense. A rational business-owner approach to looking at public and private companies.

What does change over time is the opportunities and the magnitude of things. Read about Scott Fetzer, for example. A company that nearly doubled Berkshire’s revenues and was a major contributor to its success in the ‘80s and ‘90s. That business is literally a footnote today as part of Marmon and is mentioned only once in the 2025 annual report. That’s because those businesses didn’t grow — [even though] they’re still good businesses — but Berkshire grew around it, in part funded by the cash generated from Scott Fetzer’s two dozen or so subsidiaries.

Looking back helps keep the present in context. The numbers are big today — huge, even — but consider the figures we’ll be talking about in ten or twenty years!

Q: How will the Abel era differ from the Buffett era in terms of capital allocation?

Mead: Just the sheer size of Berkshire demands a different approach to capital allocation. Berkshire can’t buy tiny businesses — and its universe of big businesses is shrinking. That said, there are huge opportunities for Berkshire.

The energy sector is going to need massive amounts of capital investment. Guess who knows that business intimately and has hundreds of billions of dollars in capital behind him? Greg Abel.

Additionally, Berkshire mainly operates in the United States. We may see more international deals along the lines of the Japanese trading houses and Tokio Marine insurance. The Abel era might just be one of global expansion as the Berkshire brand and reputation go beyond North America.

(6) Speaking of books… One of my low-key favorite things about the annual meeting is Berkshire’s list of “approved” books for sale through The Bookworm. It’s always nice to know which Berkshire-related titles get the coveted Buffett and Abel imprimatur.

Four new selections make their debut on the list this year:

1929: Inside the Greatest Crash in Wall Street History — And How It Shattered a Nation by Andrew Ross Sorkin

Streetwise: Getting To & Through Goldman Sachs by Lloyd Blankfein

Courage of a Nation: Three Years of War by Howard Buffett

Ukraine: Four Years of War by Howard Buffett

(7) On the Excess Returns podcast, Berkshire director Chris Davis talked about the conglomerate’s future. “If I could write the headline for Berkshire five years from now,” said Davis, “I would say that Berkshire was a great investment company that became a great operating company.”

For most of its modern history, Berkshire has been understood primarily through the lens of Buffett the investor. The operating businesses took a backseat in the public imagination, vessels for capital rather than the point of the enterprise. What Davis describes is a company whose center of gravity has shifted — where the subsidiaries themselves (and the people running them) become the primary story.

“You have extremely long-lived assets,” he continued. “You’ve got a very peculiar culture that is very much rational, very long-term oriented, very skeptical of Wall Street fads and mania — and run with this idea that we’re building something that has got to last through everything.”

(8) NFM store manager Scott Baker has seen it all over the years at Berkshire annual meetings. “I remember when the meeting was at the Holiday Inn Central,” he told Omaha’s KETV station, “and Warren would just pull up in this old Ford LTD and he would just go in. It’s a lot bigger deal than that now.”

That might be the understatement of the weekend.

NFM will operate a massive booth on the sales floor at CHI Health Center Arena — along with hosting a tent party at the store itself with live music and food from Weber Grill. It’s the kind of thing that makes the Berkshire AGM feel less like a run-of-the-mill shareholders meeting and more like “Woodstock for Capitalists”.

And, for Baker, that’s the entire point. “People come from all over the world to this,” he said. “It’s like a pilgrimage to come see it. We want to put our best foot forward and want people to have a good time and see what we’re [all] about.”

“I think this meeting will look very similar to previous meetings. Greg [has been] a fixture with Berkshire for a long time. Some people may skip because it’s not the Warren and Charlie show [anymore], but I also think a lot of people will come now because they want to see what Greg has to say. I think it will be a similar meeting, but you never know what’s going to happen in the future.”

(9) Bloomberg reports that Sirius XM and iHeartMedia are in preliminary talks about a possible merger. A deal would bring together the largest satellite radio service in the country with the largest terrestrial radio owner in an industry rapidly losing ground to streaming. Sirius XM and iHeart are, in different ways, the same story: legacy audio businesses built for a pre-Spotify world, now fighting for relevance against streaming platforms that have conditioned an entire generation to expect infinite music, podcasts, and audiobooks on demand.

(10) Even at 95, Warren Buffett is still winning over the critics. Billionaire hedge fund manager Paul Tudor Jones admitted recently that, for many years, he got Buffett all wrong. “I used to just sit there and rail on Warren Buffett — year after year after year,” he told the Invest Like The Best podcast. “I would self-congratulate myself for trashing him because [I thought] he just happened to be in the right place at the right time and caught this bull market.”

That’s a critique Buffett has faced from time to time. That he was simply a product of his era, who just so happened to come along and ride the greatest sustained bull market wave in American history. That’s how Tudor Jones long viewed the Oracle — but he has since reconsidered that opinion.

“What I realize now,” he said, “is what an idiot I was. That guy is a flipping genius because he understood the power of compound interest, which I somehow managed brilliantly to avoid my entire career.”

Tudor Jones also lavished praise on the other half of the Berkshire duo. “[Buffett] was so smart that he partnered with Charlie Munger,” he said. “Charlie was clearly a tremendous genius in his own right. Whereas Warren would buy fifty-cent dollars, Charlie understood the power of compounding for companies that were growing all the time. The two of them together… Man, what a combination.”

Adam Meadl second edition has a section on the Haslam and pilot j. It is another reason as Browns fans (which I think you are one) we can't get a break. I really don't think it is a flattering take on the Haslams his battle with Buffet.

I also enjoyed the very angry woman who claimed that BRK was destroying the planet! I wonder if she bought anything while she was there. A dilly bar, maybe?