Pros & Cons of P/E, Dispatches From The Streaming Wars, Disney, Marvel, Paramount, and Gary Mishuris

Happy Monday and welcome to our new subscribers!

The Plus Side of P/E…

It would be nice if there were one metric that tells investors exactly which stocks to buy and which to avoid like the plague. One number that perfectly sums up a company’s intrinsic value and makes our buy-and-sell decisions obvious.

Alas, the money game is way too complicated for that.

Some investors treat a company’s price-to-earnings (P/E) ratio as the one metric to rule them all. I get it. When researching a potential investment, its P/E ratio is usually the first number I look at — and it has certainly been known to play an outsized role in the purchase decisions of many a value investor.

Quick explainer: P/E ratio is calculated by dividing the market value (price) of a company’s shares by its earnings per share. For example, a share of Alphabet costs $2,186.26 with an EPS of $112.20. I’ll save you the math — it comes out to a 19.49 P/E.

Looking at a company’s P/E focuses the intelligent investor on one very important truth: the only thing about an investment that never changes is how much you paid for it. The price might go up on good news, earnings might soar after a particularly impressive product launch, or free cash flow could tighten due to increased capital expenditures.

All of that can — and, over the years, probably will — happen. But the one thing that will never change, will never go up or down, is how much you paid for that particular stock.

And that unchanging purchase price determines what returns you will earn on any investment.

Take one of my favorite punching bags, Cisco, for example:

In 2000, Cisco was the it stock. Analysts predicted that Cisco, like most tech stocks, was headed for the moon. And that cheery consensus resulted in a 220 P/E as speculators poured into the stock in search of quick riches. Cisco could not miss.

In 2017, on the other hand, the computer networker was a Wall Street has-been. Despite steadily growing revenue and profits over those seventeen years, Cisco traded at just 15x earnings. To many investors, especially those easily seduced by flashy start-ups, Cisco was boring. A fate worse than death.

But, all else being equal, you’d rather have bought CSCO at $30 in 2017 than at $77 in 2000. It’s the difference between a 40% gain and a 40% loss.

While analysts likely would have led you down the wrong path in both 2000 and 2017, that trusty ol’ P/E ratio could’ve saved your bacon. Cisco’s 220 P/E was a screeching alarm warning investors to seek their fortunes elsewhere. Unfortunately, too few took notice.

Sometimes, life is that easy. Avoid impossibly-high P/Es and stick to those in the sub-20 ballpark. Not a hard and fast rule, but one that will mostly keep you out of trouble.

Ultimately, that’s the power of P/E: It keeps a company’s valuation front of mind. Exactly where it should be.

…And a Few Cons

So, can a P/E ratio alone tell you which stocks to buy?

P/E is just a snapshot in time of how much you, as an investor, must pay for $1 of earnings from a particular company.

In a vacuum, it doesn’t tell you nearly as much as you might think. For “growth” companies quickly growing revenue and profits, people are willing to pay more to get a piece of that action. Hence, higher P/Es for tech companies, EV makers, and the like.

On the flip side, something like tobacco stocks — widely perceived as dying or, at best, stagnant — languish at lower P/Es because of limited upside and growth. (Not saying I agree with this assessment, but it’s reflective of the wider market’s opinion.)

To control for this, intelligent investors should mostly compare companies’ P/Es within the same industry. Be careful with crossover comparisons like judging Philip Morris (17.5 P/E) a better value than Apple (22-24 P/E). Maybe it is, maybe it isn’t — but P/E doesn’t tell the full story.

And, whenever discussing P/E, it’s important to acknowledge the times it has led value investors astray. Most notably, with Amazon.com.

Amazon’s P/E almost never falls below 50 — and has spent considerable time in the triple digits — but nevertheless delivers excellent returns to long-term investors. For years, Amazon’s earnings were depressed as the company poured immense resources into building out a massive logistics and delivery network, not to mention major investments in cloud computing. That, in turn, led to an inflated P/E.

Anyone relying on P/E analysis alone would have misjudged Amazon as overvalued.

A company’s P/E ratio is an excellent place to start researching. It’s just not a one-stop shop. Investors must dig deeper — learn about the company’s debt levels, return on capital, free cash flow, etc. — before pulling the trigger on any purchase.

Unfortunately, there’s no fool-proof statistic that takes the hard work out of this process. Investing is still more art than science.

Dispatches from the Streaming Wars, Pt. 1

Disney hasn’t enjoyed much good news lately. The company’s stock sits near multi-year lows (excluding the Covid crash) and nearly toppled below $100 per share during Friday’s erstwhile sell-off.

That’s a far cry from its 52-week high of $187.

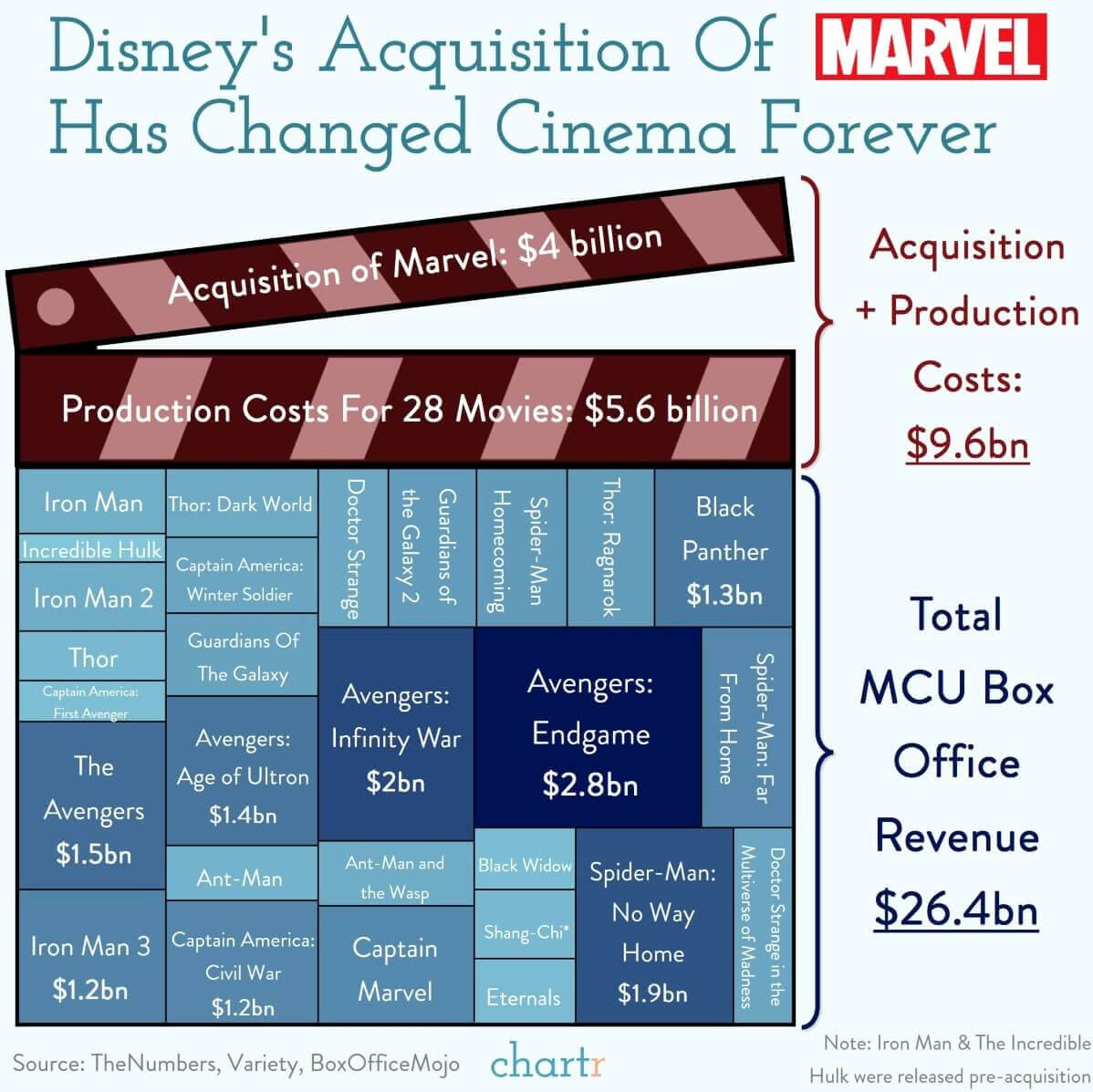

But, amidst all the doom and gloom, one ray of sunshine is poking its way through the storm clouds hanging over the Mouse. Doctor Strange in the Multiverse of Madness, the latest Marvel blockbuster, has rung up global box office receipts north of $700 million in just three weeks since release.

Disney was hit particularly hard by the pandemic. Three of the company’s major profit engines — the Disney Parks, the Disney Cruise Line, and theatrical film releases — were all shut down for months on end.

Many feared that Covid meant the end of movie theaters and that, in the future, most feature films would instead release on streaming services. It’s still early, but Doctor Strange is doing his best to dispel that notion.

Even better, the eventual move of the new Doctor Strange movie to Disney+ should be a big driver of paid subscriptions for the young streamer. Disney gets the best of both worlds: huge box office receipts from eager theatergoers and growing subs on D+.

Dispatches from the Streaming Wars, Pt. 2

Last week, Paramount CFO Naveen Chopra made an impressive appearance at MoffettNathanson’s ninth annual media and communications summit.

Some highlights from his Q&A discussion:

(1) Paramount ain’t no “legacy streamer”

Paramount’s combination of traditional media (linear television, feature film production, etc.) and streaming makes for a totally different ballgame than just pure-play streaming. Legacy assets, once derided as dying business segments, have actually turned out to be big (and profitable) plusses.

“Until very recently, the conventional wisdom was that all these traditional legacy assets are just a boat anchor to growing in streaming and you should shed them as quickly as possible and be all-in on streaming,” said Chopra.

(2) Cast a wide net for content

Chopra pointed out that legacy streamers (read: Netflix) were built on lavish scripted dramas. And those certainly don’t come cheap.

Paramount, on the other hand, hopes to leverage decades of experience in broadcast and cable television to chart a different course. One full of sports, news, unscripted (reality) shows, kids content, etc.

“Our thesis was if we can bring all of that type of content together, with scripted drama as well, into a unified streaming service, that would be a powerful draw.”

So far, so good. Chopra says Paramount+ sports content “drives the highest LTV (lifetime value) users” who are “sticky” to the service.

And Paramount’s doing just fine on the scripted drama front, too. Mostly thanks to the prolific Taylor Sheridan.

(3) Glad to have Berkshire on board

As you probably know, Warren Buffett’s Berkshire Hathaway now owns 11% of Paramount after a Q1 shopping spree. The Oracle (or Weschler/Combs) recognizes a good deal when he sees it.

“We’ve always believed there’s a lot of upside in [Paramount], so it’s certainly exciting to see someone with Berkshire’s track record see a lot of the same opportunity,” said Chopra.

But we’ll have to wait until August to see if Berkshire bought more Paramount stock during the recent dip.

Words of Wisdom from Gary Mishuris

Excellent description of the current panic and peril on Wall Street from Gary Mishuris, managing partner of Silver Ring Value Partners, in his Q1 2022 letter:

As the market bubble is being dragged, kicking and screaming, to its deathbed, the speculators and bull-market players are starting to get shell-shocked. Having thought themselves to be master stock pickers in an environment where the universe from which they were selecting investments had produced 25% annual returns, they are now staring at losses in the range of 25% to 50%, with likely more to come. Behaviorally, that is a very challenging situation in which to remain rational and make good investing decisions for the future.

If you enjoy my work, please hit the ❤️ below and share this post with anyone who might be interested (or on social media). Thank you!

Disclosure: This is not financial advice. I am not a financial advisor. Do your own research before making any investment decisions.