Greg Abel Enters The Arena

"One of our greatest strengths at Berkshire is patience."

At this weekend’s Berkshire Hathaway annual shareholders meeting, new CEO Greg Abel didn’t try to be Warren Buffett.

He did something harder.

He proved he doesn’t need to be.

For decades, the Berkshire AGM was geared around two singular personalities — Warren Buffett and Charlie Munger — whose wit, candor, and accumulated wisdom made the gathering something between an investment masterclass and a secular pilgrimage. This year, with Charlie gone and Warren sitting off stage, this festival of capitalism had to forge a new identity.

And I think Abel gave it one.

Rather than reach for Buffett’s philosophical fireside manner, Abel offered something different — depth, detail, and a commanding operational fluency across the far-flung corners of the conglomerate. Where Buffett dazzled with aphorism and analogy, Abel impressed with granular specificity and a clear vision for what comes next.

It felt, at times, like drinking from a firehose. A long, substantive immersion in Berkshire’s many businesses — the kind that had faded a bit in recent years as Warren and Charlie embraced their roles as elder statesmen opining on loftier subjects.

Whether Abel was describing how Berkshire’s metals businesses fit together, laying out a roadmap for “Narrow AI” at BNSF Railway (and beyond), or dissecting the regulatory friction currently hampering Berkshire Hathaway Energy — the man had clearly done his homework.

“That is Greg’s wheelhouse,” said director Chris Davis. “He’s just a fabulous operator.”

“He knows these businesses like the back of his hand,” agreed Occidental Petroleum CEO Vicki Hollub during the CNBC halftime show.

Former Activision Blizzard CEO Bobby Kotick put it simply: “I love the fact that they are actually doing more of a deep dive into the businesses. You’re never going to replace the Warren and Charlie dynamic, [so] I think that’s a great pivot.”

I always felt like I learned something new from Warren and Charlie at the AGM.

And, happily, that tradition seems to be in safe hands.

Warren Buffett may not have been on stage — but he was everywhere else.

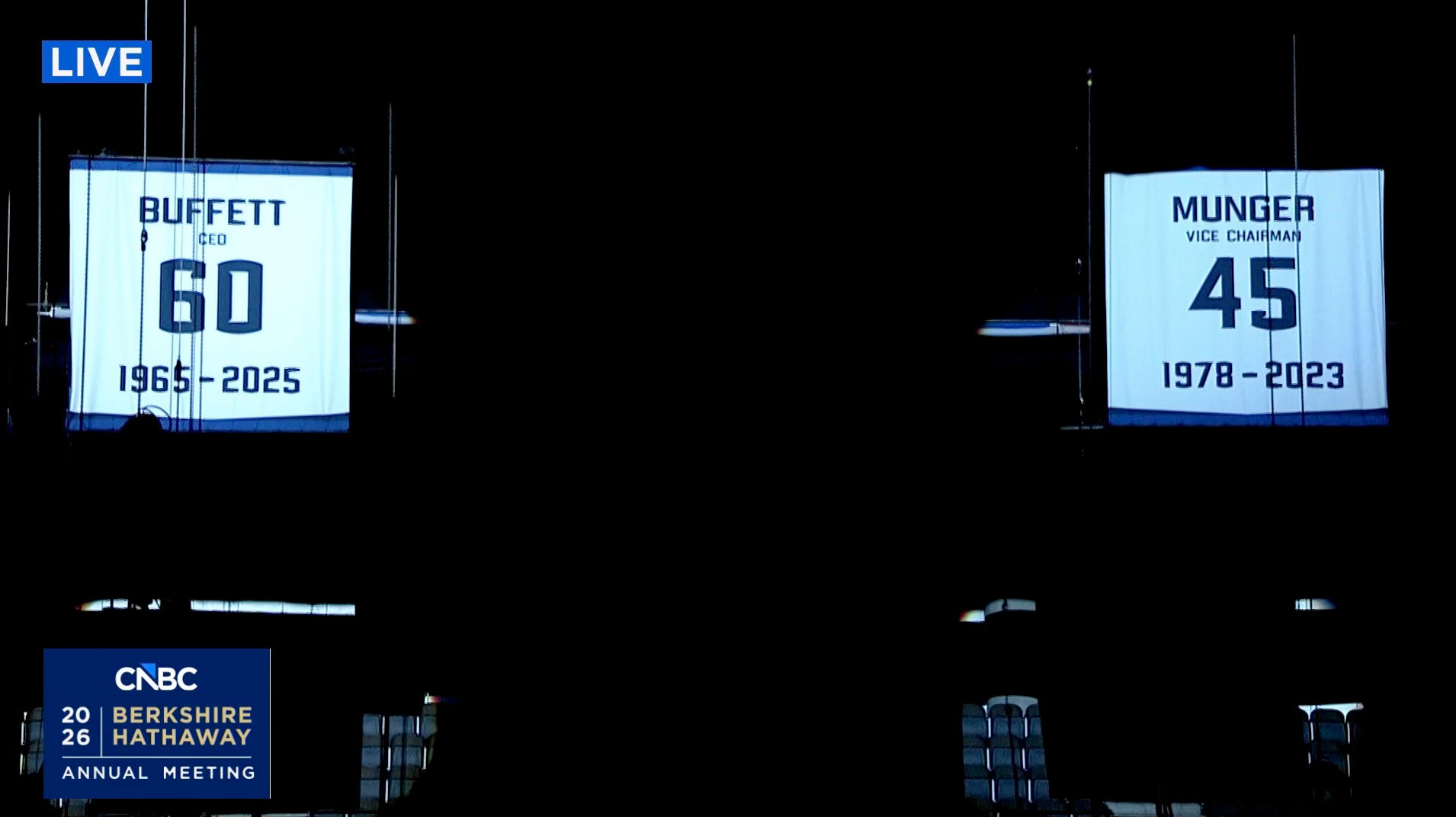

Berkshire Hathaway wisely wove the retired Oracle into the day’s events as much as humanly possible. The meeting opened with Greg Abel retiring Buffett’s “number” in the rafters of the CHI Health Center Arena, alongside Charlie Munger’s.

From his front-row seat, Buffett then grabbed the microphone and offered his verdict on his successor — “He’s very, very, very smart about businesses” — before labeling the entire leadership transition “100% successful”.

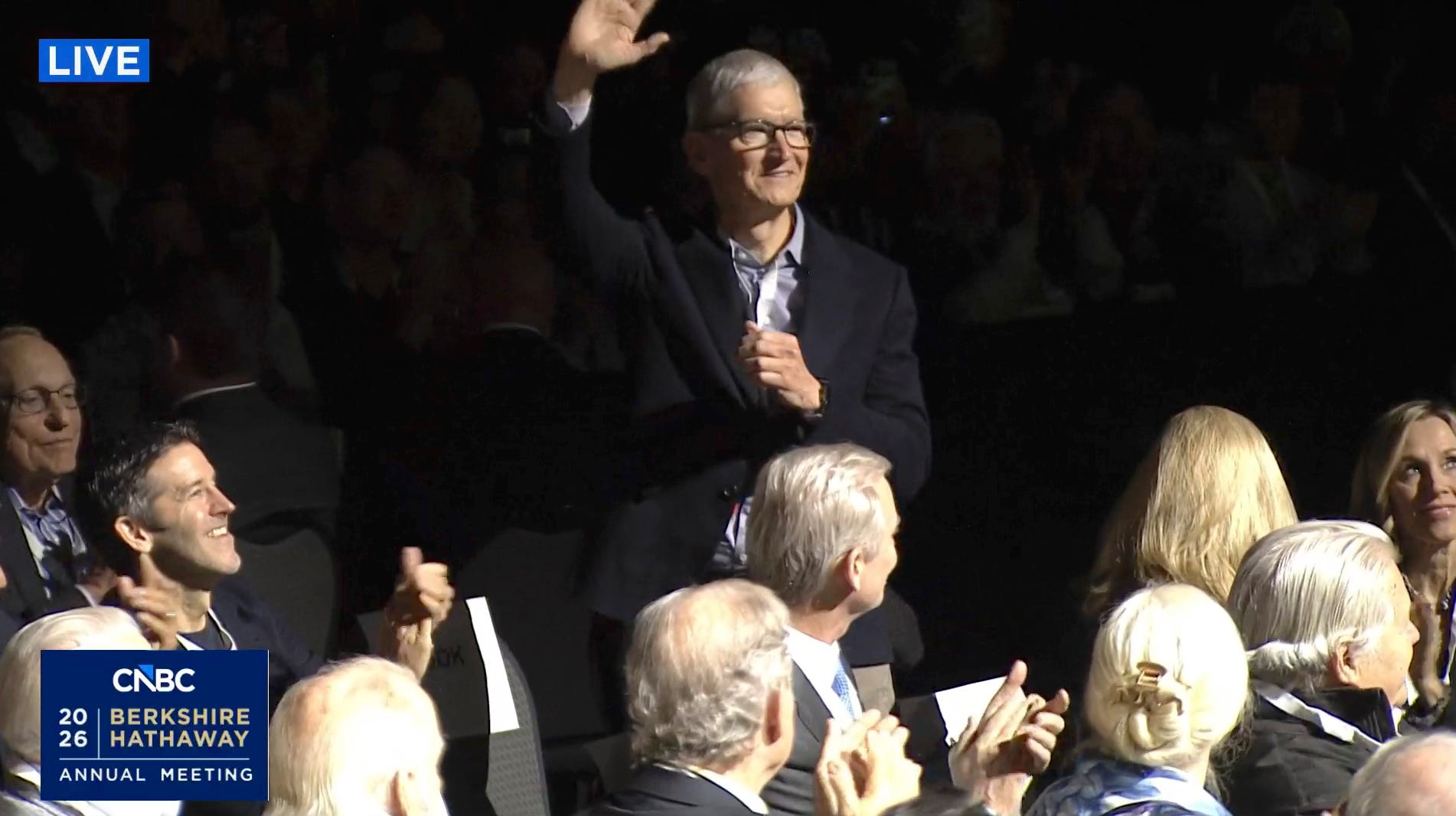

Before turning the spotlight back over to Abel, he also asked retiring Apple CEO Tim Cook to take a bow for stewarding Berkshire’s biggest investment so well. (FYI: That’s incoming CEO John Ternus sitting to the left of Cook.)

Abel, for his part, joked that after Buffett’s surprise retirement announcement last year, he half-expected only the board and his family to show up at the 2026 meeting. The crowd was indeed lighter — inevitable, given the circumstances — but I imagine everyone in attendance was thrilled to see Buffett still playing a biggish role.

After Abel wrapped up his “very fulsome” business update, an AI deepfake of Buffett asked the first question of the Q&A session. Which was either a charming tribute or a mild existential provocation — depending on your disposition.

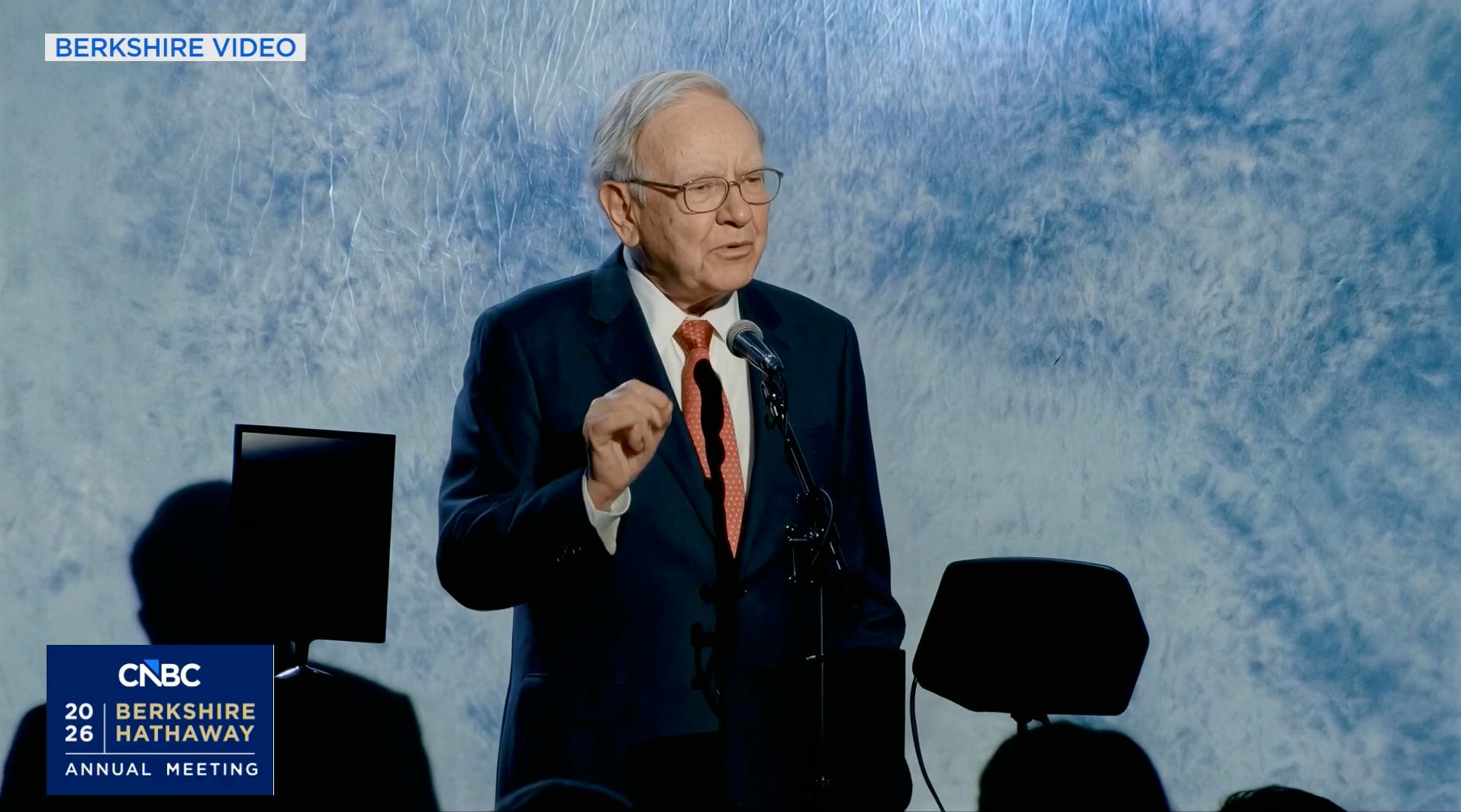

Finally, backstage, Buffett sat for a 25-minute interview with Becky Quick after the lunch break — and delivered some vintage wisdom.

“It isn’t our ideal environment in terms of deploying cash for Berkshire,” he said. “We can pick our spots and nobody can tell us what to do exactly — so sometimes we’re doing nothing. But, other times, we get quite active.”

“Of the sixty years I’ve been in the business,” he added, “probably [only] five of them have been really juicy.”

Berkshire Hathaway has never felt an urgency to act for the sake of acting — and that doesn’t look to be changing any time soon.

I don’t get the sense that the conglomerate’s $380 billion will burn a hole in Greg Abel’s pocket any faster than it did for Warren Buffett. He made clear that Berkshire’s culture — its refusal to be rushed, its allergy to ego-driven dealmaking — is no relic of the Buffett era. But something to be nurtured and cultivated for decades to come.

Abel invoked his predecessor’s legendary congressional testimony during the Salomon Brothers scandal — “Lose money for the firm and I will be understanding, [but] lose a shred of reputation and I will be ruthless” — and declared it Berkshire’s “anthem” for all time.

“We do not intend to [ever] be beholden to anyone,” said Abel of the company’s massive cash pile. But he also pledged to “act decisively and with significant capital” when the right buying moment arrives. “One of our greatest strengths at Berkshire is patience.” Enough said.

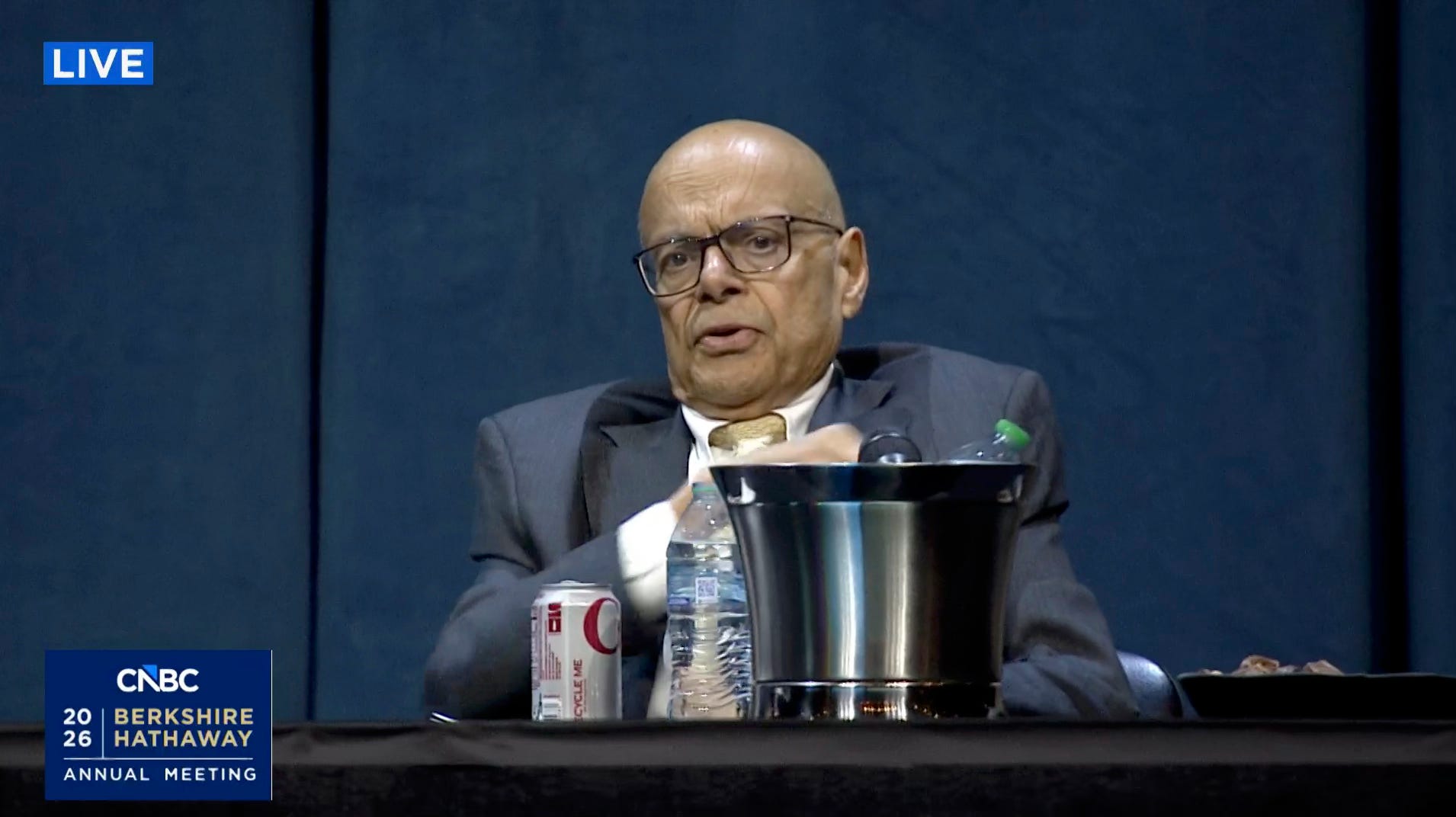

Vice chairman of insurance operations Ajit Jain and Abel — who shared an easy rapport together on stage — both made the same essential argument: saying no to almost everything is what makes the rare yes so powerful. “Insurance,” said Jain, “much like investing, is a game that requires patience. It is very difficult to get people to sit back and do nothing.” He even structures insurance compensation so that underwriters are not financially disadvantaged for not writing business.

Abel recounted a proud moment when, during a deposition, someone asked the witness to describe him as a CEO and manager. “Well,” the person replied, “all [Greg ever] says is no.” We might have a new Abominable No-Man on our hands. Somewhere out there, Charlie is smiling.

Greg Abel used the term “operational excellence” several times on Saturday.

And, in the run-up to the annual meeting, lead director Sue Decker explained why that particular emphasis could pay big dividends in the future. “The company has grown so much,” she told CNBC, “that what has become more important is growing the operating earnings versus the capital allocation piece of this.”

“If you think about the operating earnings now are $45 billion after tax — and a 12% increase on that is $5.5 billion. That’s as much as Burlington Northern makes a year. So just having the focus on execution and growing those operating earnings can add a Burlington Northern every year without making an acquisition.”

She invoked the Steve Jobs ➡️ Tim Cook parallel to hammer home her point.

“[Cook] didn’t try to be a better Steve Jobs,” said Decker. “Steve laid a great foundation and he scaled it and grew the market cap from $350 billion to $4 trillion now. 10x. That speaks to the fact that the right leader, at any given time, may change based on the operating conditions of the company. Warren has handed Greg an incredible foundation and now he needs to compound that by improving the operations.”

The era of Warren Buffett and Charlie Munger is irreplaceable. No one argues that. But what this weekend showed is that this next chapter will have its own distinct logic and someone at the top with a vision for the future. Abel is no philosopher-king, but an operator’s operator. A man who spent decades learning Berkshire from the inside out, subsidiary by subsidiary, deal by deal. I can’t wait to see how it all turns out.

It is a mixed feeling to see how the Buffett era is really closing its chapter, and it is exciting to see how Abel will turn out to be. I saw the cash pile and how people always see how ridiculous it is to hold it during this time, but I think I remember somewhere I read that Berkshire is like a 1-800 number; they don't always call it, but it exists for a reason. And that cash pile is actually in T-Bills and keeps generating interest.

Thanks, Kevin for another fine summary.

I have two takeaways for us as investors:

1. Ajit’s reference to guiding insurance underwriters to feel comfortable saying no. To help in-force this he pays them salaries, rather than performance bonuses that might incentivize them to write poor policies. That relates to us as investors managing other people’s money. It is too easy for us to feel we should be fully invested. Imagine being 30% in cash, because there are no acceptable investments. Both Warren and now Greg are comfortable sitting on cash.

2. In his interview with Becky, Warren noted that the market has moved from being speculative to gambling. Many investors seem to think that if something doubled in price, it will double again, like betting on a winning horse.

Keep at it!