Before Berkshire: Warren Buffett's Tab Card Triumph

In 2008, Alice Schroeder provided an invaluable glimpse at Buffett’s decision-making process when evaluating a new business

A recurring theme of Warren Buffett’s annual letters over the years is that he eats his own cooking. Virtually his entire net worth has been invested in Berkshire Hathaway — and, before that, his investment partnership — for nigh on seventy years.

One notable exception — which he mentioned a few times in said letters — was his “continued holding of Mid-Continent Tab Card Co., a local company into which I bought in 1960 when it had less than 10 stockholders”.

On the surface, this sounds like a decidedly un-Buffett-like investment. Why would the famously tech-averse investor plunge his own money into a company so closely intertwined with the fledgling computer industry?

For many years, it remained a mystery.

But that all changed in 2008.

Buffett biographer Alice Schroeder spoke on the opening night of that year’s Value Investing Conference at the University of Virginia and shed some much-needed light on this little-known investment.

And, in the process, provided an invaluable peek behind the curtain at Buffett’s decision-making process when evaluating a new business.

For posterity and future study, I’ve transcribed Alice Schroeder’s remarks from that evening about Warren Buffett and the Mid-Continent Tab Card Co.

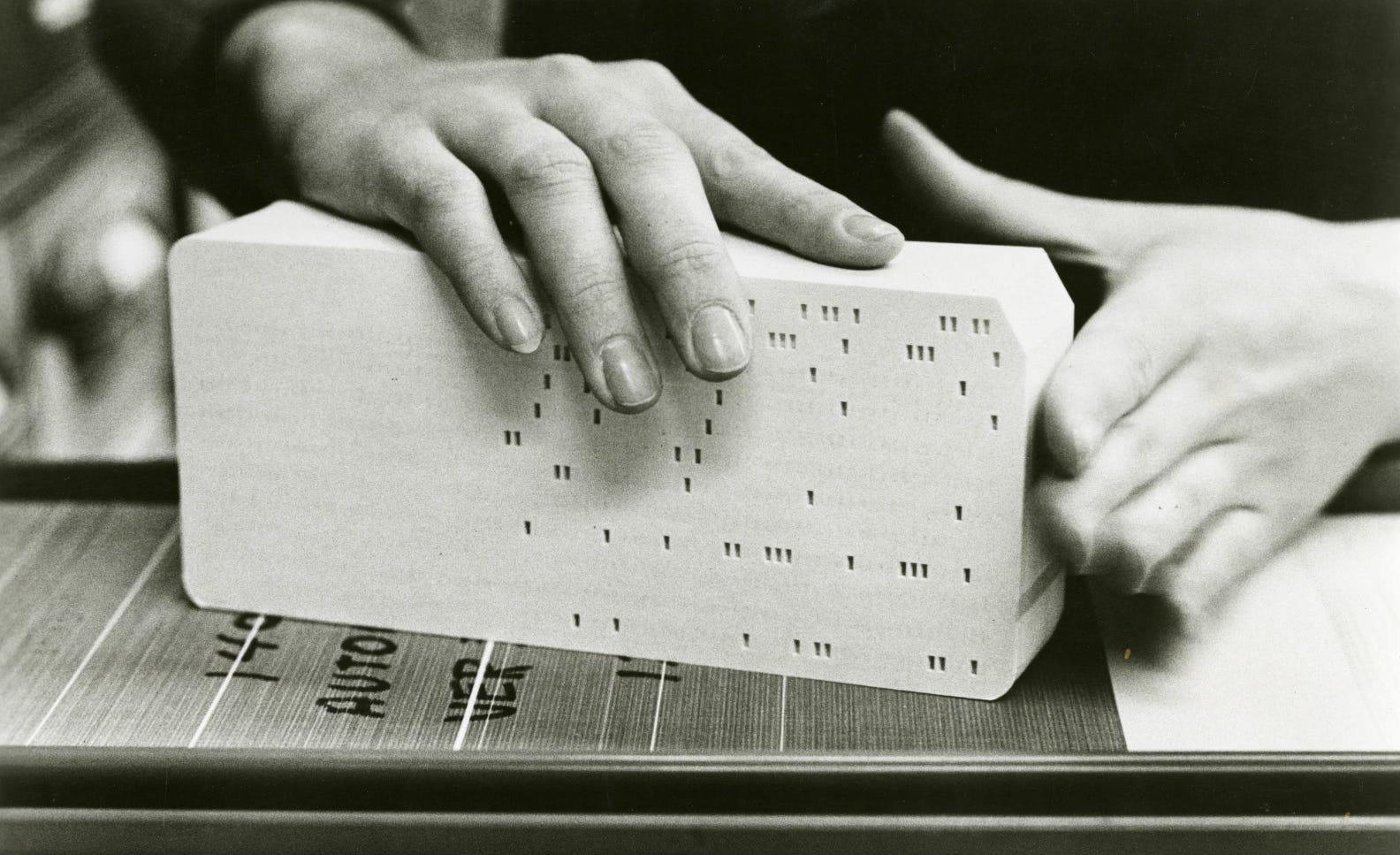

Schroeder: Before computers were digital, they actually read off of punch cards. They were called “mark sense" cards and these were big decks of cards that had holes punched in them. They would be stuck in the computer — they were not electronic — [and] they were sent mechanically through the computer.

This company was formed because IBM had to divest of this business. It was an incredibly, incredibly profitable business. In fact, because these cards were trivial compared to the mainframe computers that IBM sold, it marked them up to get more than a 50% profit margin. This was IBM’s most profitable business.

So Wayne Eaves and John Cleary, who were two friends of Warren’s, saw that IBM was going to have to divest in this business and they thought: We’re going to buy a Carroll press — which was the press that makes these cards — and we’re going to compete with IBM because we’re based in the Midwest, we can ship faster, [and] we can provide better service.

They went to Warren and they said, “Should we invest in this company and would you come in with us?” And Warren said no.

Why did he say no?

He didn’t say no because it was a technology company. He said no because he went through the first step in his investing process. And this is where, I think, what he does that’s very automatic — but isn’t well understood. He acted like a horse handicapper.

The first step in Warren’s investing process is always to say, “What are the odds that this business could be subject to any kind of catastrophe risk that could make it just fail?” If there is any chance that any significant amount of his capital could be subject to catastrophe risk, he just stops thinking. No. And he won’t go there.

It’s backwards [to] the way that most people invest because most people find an interesting idea, they figure out the math, they look at the financials, they do a projection, and then at the end they ask themselves, “Okay, what could go wrong?”

Warren starts with what could go wrong. Here, he said a start-up business competing with IBM could fail. Nope. Sorry. And he didn’t think another thing about it.

But Wayne Eaves and John Cleary went ahead anyway. They started up this business and, within a year, they were printing 35 million tab cards a month. So, at that point, they needed to buy more Carroll presses and they came back to Warren and they said, “We need money. Would you like to come in?”

Okay, so now Warren is interested because the catastrophe risk element of the equation is gone. They are competing successfully against IBM.

He asked for the numbers and they explained to him that they were turning their capital over 7x a year. A Carroll press cost $78,000 [and] every time they run a set of cards through it and turn their capital over, they are making over $11,000. So basically their gross profit a year on a press is enough to buy another printing press.

At this point, Warren is very interested. Their net profit margins are 40%. It’s like the most profitable business that he’s ever had the opportunity to invest in.

Notably, people are now bringing Warren special deals. It’s 1959 and he’s been in business for two-and-a-half years running the partnership. Why are they doing that? It’s not because they know he’s a great stock picker. They don’t know that. He hasn’t yet made that record. It’s because he knows so much about business and, because he started so early, that he has a lot of money.

This is something interesting about Warren Buffett. By 1959, people were already bringing him special deals — like they’re still doing today with Goldman and GE.

He decided that he would come in and invest in this company — Mid-Continent Tab Card Co. — but, interestingly, he did not take Wayne and John’s word for it. The numbers they gave him were really enticing, but again he went through and he acted like a horse handicapper.

Here’s another point of departure from what almost anybody else would do. Everybody that I know — or knew as an analyst — would have created a model for this company and would have projected out its earnings and would have looked at its return on investment in the future. Warren didn’t do that. In fact, in going through hundreds of his files, I’ve never seen anything that resembled a model.

What he did is he did what you would do with a horse. He figured out the one or two factors that could make the horse succeed or fail — and, in this case, it was sales growth and making the cost advantage continue to work. Then, he took all of the historical data, quarter by quarter for every single plant, he got the similar information as best he could from every competitor they had, and he filled pages with little hen scratches of all this information and he studied that information.

And, then, he made a yes/no decision. He looked at it: They were getting 36% margins [and] they were growing over 70% a year on a million of sales. Those were the historic numbers. He looked at them in great detail — just like a horse handicapper studying the tip sheet — and then he said to himself, “I want a 15% return on $2 million of sales.” And then he said, “Yeah, I can get that.” And he came in as an investor.

So what he did is he incorporated his whole earnings model and compounding discounted cash flow into that one sentence. “I want 15% on $2 million of sales.”

Why 15%? Because Warren is not greedy. He always wants a mere 15% day one return on an investment and then it compounds from there. That’s all he has ever wanted. He’s happy with that. It’s a very simple thing. There’s nothing fancy about it.

I think that’s another important lesson because he’s a very simple guy. He doesn’t do any kind of discounted cash flow models or anything like that. For decades, he just says, “I want a 15% day one return on my investment and I want it to grow from there.” Ta da!

The $2 million of sales was pretty simple, too. It had $1 million [and] it was growing 70%. There was a big margin of safety built into these numbers. It had a 36% profit margin and he said, “I’ll take half that.”

He ended up putting $60,000 of his personal non-partnership money into this company, which was about 20% of his net worth at the time. He got 16% of the company’s stock, plus some subordinated notes.

The way he thought about it was really simple. It was a one-step decision. He looked at historical data and then he had this generic return that he wants on everything. It was a very easy decision for him — and he relied totally on historical figures with no projections. I think that that’s a really interesting way to look at it because I saw him do it over and over in different investments.

So what happened? The company changed its name to Data Documents. He owned the investment for 18 years. He ended up putting another $1 million into it over time. It was bought out by Dictograph in 1979 and he earned a 33% compounded return over the 18 years that he owned the investment. So it was not too bad.

And that was typical. I gave you this example in part because it was the other time besides GEICO that he got a Phil Fisher-type growth company at a Ben Graham-like price. It was the most vivid example of that that I found, but it was a private investment and there’s not a lot of public information about it available.

A member of the audience later asked Schroeder about Buffett’s “pages with little hen scratches” of all the information he gathered on Mid-Continent Tab Card Co. before reaching his decision.

Schroeder: What you would see is a column that said “Sales” and a column that said “Expenses” and a column that said “Profits”. It would have the Louisville plant, the Kansas City plant, this plant, that plant — and it would have first quarter, second quarter, third quarter, fourth quarter 1958, [etc.] And then it would end with the last quarter that was reported. That’s what his is. That’s all it is.

The difference from a model is [Buffett’s] would not add the quarters up and it would not project anything into the future. Nothing.

In other words, he looked at what had been reported and he said, “They’ve had a million in sales. They’ve earned this many thousand. I want this much. They’ve earned this and I want this. Can they do it? Yes [or] no.” That’s the decision.

There’s a saying — I think it’s from The Intelligent Investor — that the purpose of the margin of safety is to render forecasts unnecessary.

Quite a nugget about what Buffett was looking in an investment. Time to reread The Snowball. Thanks for sharing.

Another saying is to the tune of; "only invests when one buys historical corporate activity at a discount and capture its future for free".