A Closer Look at Warren Buffett's 2024 Annual Letter to Shareholders

“Berkshire’s activities now impact all corners of our country," wrote Buffett. "And we are not finished."

Warren Buffett released his much-anticipated annual letter to Berkshire Hathaway shareholders over the weekend.

Perhaps the most striking thing about this year’s letter is how normal it is. No dividend announcement, no retirement plans, not even much discussion about Berkshire’s mammoth (and growing) cash position.

It’s all very much business as usual for Buffett.

Which, considering we’re talking about a 94-year-old here, is a good thing.

Buffett’s annual letters now land on the short-and-sweet side of the fence — especially compared to the lengthy reflections of his earlier days. And while I cherish those longer letters and their life-changing wisdom, I can’t begrudge the man for whittling down the ol’ word count a bit. After decades of writing, there surely comes a time when you’ve already said exactly what you needed to say — and anything more would just be padding.

Today, I’d like to take a closer look at a few of the more important concepts from Buffett’s newest letter. And how, even after sixty years at the helm of Berkshire, the old man is still surprising us.

Berkshire Hathaway in 2024

“In 2024,” wrote Buffett, “Berkshire did better than I expected — though 53% of our 189 operating businesses reported a decline in earnings.”

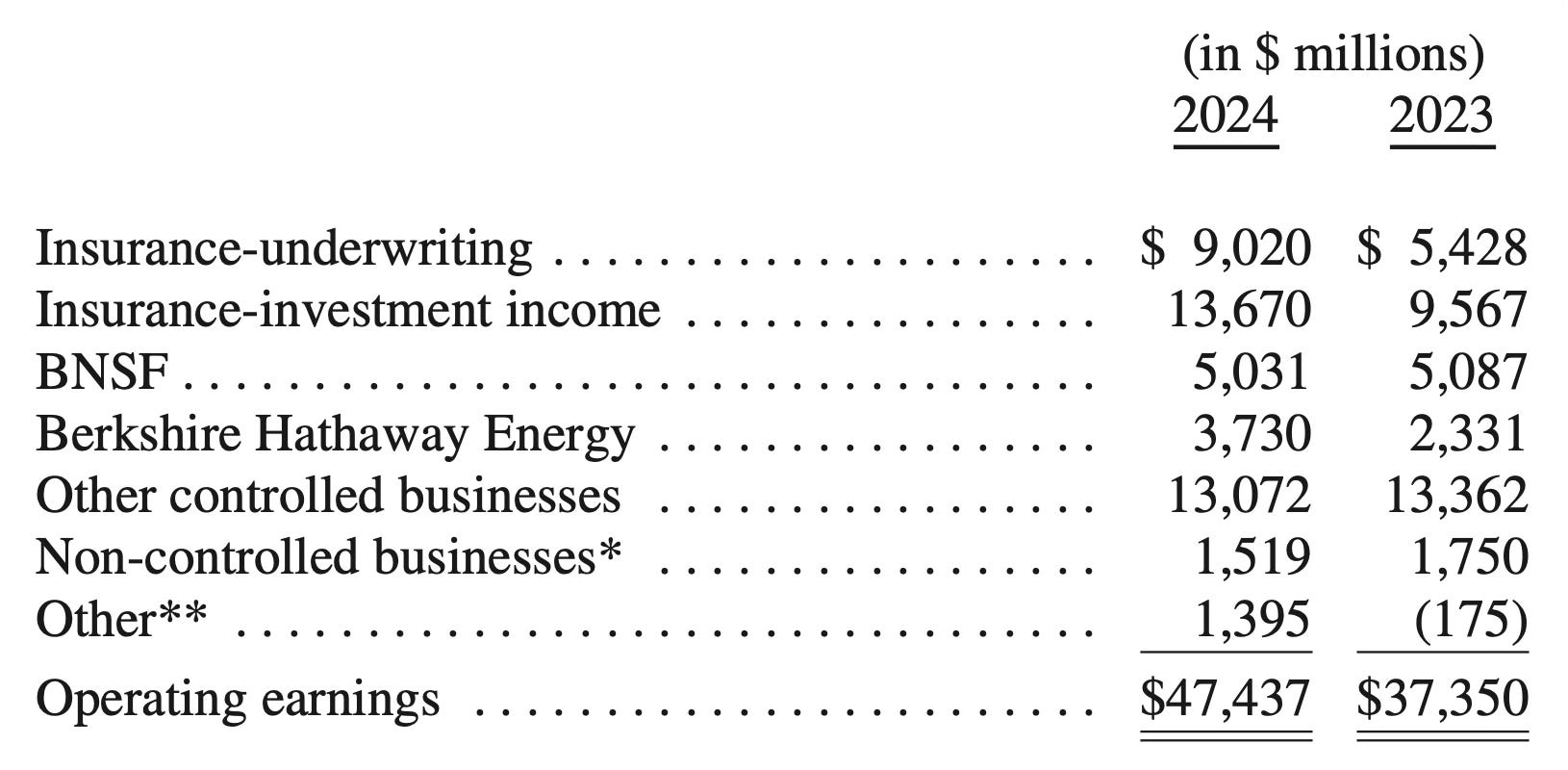

Berkshire recorded $47.4 billion in operating earnings last year — which remains Buffett’s preferred measure of the conglomerate’s performance. It avoids the wild swings that show up in GAAP earnings when the conglomerate’s massive stock portfolio gets marked to market each quarter whether any shares were sold or not.

Here is how the various pieces and parts of the Berkshire machine functioned in 2024. “All calculations are after depreciation, amortization, and income tax,” said Buffett. “EBITDA, a flawed favorite of Wall Street, is not for us.”

Well, at least that’s nicer than what Charlie would have said…

Buffett heaped particular praise on Todd Combs for his role in resuscitating GEICO. The auto insurer posted an impressive 81.5% combined ratio in 2024 and more than doubled its pre-tax underwriting earnings year over year.

“In five years,” wrote Buffett, “Todd Combs has reshaped GEICO in a major way, increasing efficiency and bringing underwriting practices up to date. GEICO was a long-held gem that needed major re-polishing and Todd has worked tirelessly in getting the job done.”

BNSF Railway and Berkshire Hathaway Energy, meanwhile, received better reviews than last year — but are not fully on track just yet. “Berkshire’s railroad and utility operations, our two largest businesses outside of insurance, improved their aggregate earnings. Both, however, have much left to accomplish.”

That Cash Pile

I think everyone expected Berkshire Hathaway’s cash position — which, again, grew still larger in the fourth quarter — to be a major topic of this year’s annual letter.

But that’s not quite what happened.

Buffett didn’t ignore the subject, but he didn’t feel compelled to offer any explanation or defense for Berkshire’s cash, either. “Despite what some commentators currently view as an extraordinary cash position at Berkshire,” he wrote, “the great majority of your money remains in equities.”

He explained that Berkshire’s “ambidextrous” strategy — whether it’s purchasing stock on the open market or acquiring a business outright — affords him the flexibility to allocate capital towards whichever “equity vehicle” looks more attractive at any given time.

“Really outstanding businesses are very seldom offered in their entirety, but small fractions of these gems can be purchased Monday through Friday on Wall Street and, very occasionally, they sell at bargain prices.”

“Often,” he lamented, “nothing looks compelling; very infrequently we find ourselves knee-deep in opportunities.”

Left unsaid is that we seem to be in one of those “nothing compelling” times.

As such, Berkshire’s cash number grew to $318 billion at year end. (I don’t typically include cash from Railroad, Utilities, & Energy in this total — and there’s $12.8 billion payable for U.S. Treasury Bills to subtract, too — so you might see a bigger number elsewhere.) Cash now represents 27.6% of Berkshire’s total assets.

Buffett, though, does not sound overly concerned about that fact.

And if he’s not worried, I’m not worried.

While some people angst over Berkshire holding so much cash — and plenty felt this way when the number was $100 billion, let alone $318 billion — I rest easy knowing that Buffett has a war chest of epic proportions with which to operate.

Three Cheers for Greg Abel

The only very slight hint towards the inevitable changes ahead for Berkshire came in Buffett’s more frequent mentions of vice chairman (and heir to the throne) Greg Abel.

On three separate occasions in this year’s letter, Buffett shared asides about Abel and his managerial abilities. Every time I learn something new about Greg, I feel more and more confident about the post-Buffett era.

While discussing Berkshire’s capital allocation in both stocks and subsidiaries, Buffett credited Abel with a Munger-like ability to wait patiently for the right opportunity — and then aggressively pounce on it in a big way. “Greg has vividly shown his ability to act at such times as did Charlie,” wrote Buffett. Praise doesn’t come much higher than that.

Buffett devoted an entire section of his letter to Berkshire’s investments in the five Japanese trading houses. “As the years have passed,” wrote Buffett, “our admiration for these companies has consistently grown. Greg has met many times with them and I regularly follow their progress.”

He also revealed that the sogo shosha agreed to “moderately relax” the agreement that limited Berkshire to 9.9% ownership in each — leading Buffett to say that Berkshire “will likely” buy more of each. And he reiterated that this foray into Japan is for the very long haul. “I expect that Greg and his eventual successors will be holding this Japanese position for many decades and that Berkshire will find other ways to work productively with the five companies in the future.”

Buffett reminded us that a “report” from management to shareholders cannot mince words or hide inconvenient truths. The Berkshire 10-K has never been about “happy talk and pictures” — and that will not change under Abel’s watch. “At 94,” wrote Buffett, “it won’t be long before Greg Abel replaces me as CEO and will be writing the annual letters. Greg shares the Berkshire creed that a ‘report’ is what a Berkshire CEO annually owes to owners. And he also understands that if you start fooling your shareholders, you will soon believe your own baloney and be fooling yourself as well.”

P/C Insurance

Property/casualty insurance — which Buffett called “Berkshire’s core business” — is quite unlike other businesses. While most companies know their costs upfront and then sell products or services at a price that covers said costs, insurance is different. Premiums are written — and cash received — long before anyone knows for certain what the coverage will end up costing the insurer. In some cases, it takes decades.

This heaps immense importance on the integrity and discipline of underwriters. It’s frightfully easy to — knowingly or unknowingly — take bad risks, collect money from customers, and delude yourself into believing that all is well. Meanwhile, the company is actually on a slow march to the gallows.

“[An insurer] can be losing money — sometimes mountains of money — before the CEO and directors realize what is happening,” wrote Buffett.

Which goes a long way towards explaining how much Ajit Jain has meant to Berkshire over the past four decades. He oversees this dangerous tightrope walk between risk and growth — and has done so in a way that has added countless billions of dollars to Berkshire’s bottom line.

The man that brought Ajit to Berkshire — Mike Goldberg — also got a much-deserved shoutout in this year’s letter. Buffett quoted him as saying, “We want our underwriters to daily come to work nervous, but not paralyzed.”

A Few More Great Lines…

“Our experience is that a single winning decision can make a breathtaking difference over time.”

“The cardinal sin is delaying the correction of mistakes or what Charlie Munger called ‘thumb-sucking’. Problems, he would tell me, cannot be wished away. They require action, however uncomfortable that may be.”

“I never look at where a [CEO] candidate has gone to school. Never!”

“From a base of only four million people — and despite a brutal internal war early on, pitting one American against another — America changed the world in the blink of a celestial eye.” 🇺🇸

“The sensible — better yet imaginative — deployment of savings by citizens is required to propel an ever-growing societal output of desired goods and services. This system is called capitalism. It has its faults and abuses … but it also can work wonders unmatched by other economic systems.”

“Berkshire’s activities now impact all corners of our country. And we are not finished. Companies die for many reasons but, unlike the fate of humans, old age is not lethal. Berkshire today is far more youthful than it was in 1965.”

Warren Buffet, phenomenal wealth creation in one generation combined with a high moral compass. Someone to model & emulate.

As part of the human condition power seems to corrupt in many cases. Power does not seem to have corrupted Warren Buffet. Stay strong 💪

Ever sober. Ever wise. 'Nuff said.