A Closer Look at Berkshire Hathaway's Q1 2025 Earnings Report

All of the little (and big) details from Berkshire's latest 10-Q

On May 3, just a few hours before Warren Buffett announced that he will step down as CEO at year’s end, Berkshire Hathaway released its Q1 2025 earnings report.

And, understandably, Buffett’s big moment stole the spotlight from these numbers.

So today is all about circling back and taking a closer look at Berkshire’s performance in the first quarter. Let’s dive in…

First Things First

Warren Buffett and Charlie Munger always championed Berkshire Hathaway’s operating earnings as the best way to take the pulse of the conglomerate. These earnings fell 14.1% in the first quarter, a seemingly steep decline that is perhaps not all that it seems at first glance. If you strip out the fluctuations from foreign currency exchange — removing the $713 million “loss” in Q1 2025 and the $597 million “gain” in 2024 — Berkshire’s operating earnings dipped just 2.6% instead.

Cash flows from operating activities increased by $337 million to $10.9 billion.

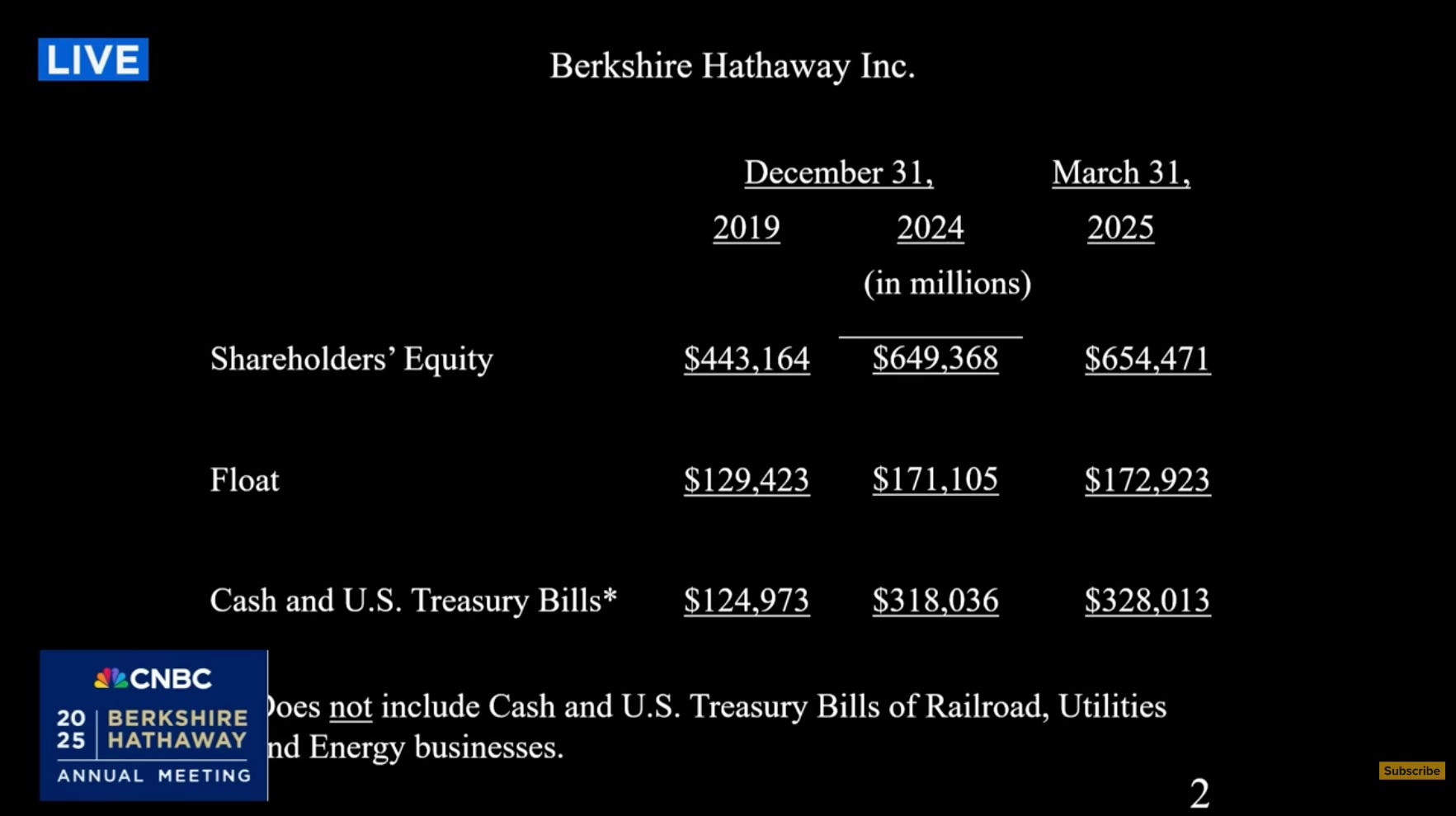

Berkshire’s cash mountain grew to a staggering $328 billion — after subtracting out $14.4 billion payable for purchases of U.S. Treasury Bills. (And not including any cash in Railroad, Utilities, and Energy.) This is how Buffett himself calculates Berkshire’s cash total, as seen in this slide from the annual shareholders meeting.

“[Berkshire] continues to hold a lot more in cash and Treasury Bills than I would like,” said Buffett, “but that’s simply a question of when opportunities occur.” Such opportunities don’t come around every day — though Buffett did tantalizingly reveal that he came close to spending $10 billion on something in the first quarter.

The complete lack of share repurchases further fueled this cash build-up. Berkshire’s Class A equivalents remain at 1,438,223 shares — with no buyback activity during the first few weeks of April, either. Buffett noted that the 1% excise tax on share repurchases (which went into effect in 2023) made this capital allocation strategy less attractive than it once was.

Berkshire kept us all guessing about its Q1 2025 investment activity — breaking tradition by omitting the end-of-quarter values for its top five equity holdings. The five stocks in question did not change — still Apple, American Express, Bank of America, Coca-Cola, and Chevron — but we’ll have to wait for the 13F on Thursday to see if Buffett tinkered with any of them.

For the tenth quarter in a row, Berkshire was a net seller of stocks — with $4.7 billion in sales and $3.2 billion in purchases.

Insurance

Insurance underwriting slumped by $1.26 billion in the first quarter — weighed down by $860 million of after-tax losses from the Southern California wildfires in January. Plus, last year’s numbers were a very tough act to follow. “Our insurance underwriting income was down dramatically for the first quarter,” said Buffett. “Last year was as good a year as you’ll see in insurance. It’s always unpredictable, but everything broke our way — or the insurance industry’s way — last year.”

GEICO defied the downturn with a $245 million boost in pre-tax earnings — fueled by a scarcely-believable 79.8% combined ratio. (The lower the better, as anything under 100% represents an underwriting profit.) Ajit Jain gushed that he never thought he would live to see the day that any insurer could get its combined ratio as low as GEICO’s right now. Take a bow, CEO Todd Combs.

Even more impressive, GEICO posted these numbers while increasing underwriting expenses from $892 million to $1.15 billion. Mainly policy acquisition-related expenses, resulting in an increase in policies-in-force. GEICO is back in growth mode.

The Primary and Reinsurance segments both posted modest pre-tax losses. Over in Primary, loss expenses ballooned by $640 million in the quarter — resulting in a subpar 103.1% combined ratio. Reinsurance took a big hit from the SoCal wildfires, but foreign exchange currency losses also took a toll on the bottom line. In fact, if you factor out for-ex, Reinsurance’s underwriting expenses actually declined by 2.3% in the quarter.

On the investment side, income grew by $295 million as Berkshire parked more and more of its cash in Treasuries. “Rates on short-term bills are less than they were before,” said Buffett, “so you had that negative effect pulling it down — but not that much. And we had more money [invested in these bills] so we came up with a little more in the way of earnings.”

Berkshire’s float inched up to $173 billion. And, since underwriting continues to be profitable, this is effectively free money that Buffett and co. can put to work as they see fit until insurance claims come due. Ajit noted that this amount of float is “head and shoulders above anyone else” in the industry.

BNSF Railway

BNSF’s net earnings increased by 6.2% in the first quarter. A 4.1% boost in unit volume drove these results — with consumer products leading the way at 8.6% and even coal getting in on the act with a 1.7% increase. On the downside, agricultural and industrial products declined in volume — and severe weather in February also negatively affected the railroad’s performance.

“It’s not earning what it should be earning at the present time,” said Buffett, “but that’s solvable — and is getting solved.” Nevertheless, he still considers BNSF an “incredible” asset for Berkshire.

Berkshire Hathaway Energy

Berkshire Hathaway Energy roared back with a 53% jump in net earnings — going from $717 million a year ago to $1.1 billion now.

U.S. utilities increased by 13.8% on higher retail customer rates and volume. (MidAmerican Energy boosted customer volume by 11.3%, PacifiCorp 2.4%, and NV Energy 0.8%.)

Natural gas pipelines declined 2.2% on lower margins and higher interest expense. The latter resulted from debt issued in January and other refinancing late last year at higher interest rates.

Other energy businesses surged 23% on higher earnings from Northern Powergrid across the pond.

The real estate brokerage sharply reduced its losses ($159 million in Q1 2024 to just $15 million in Q1 2025) as litigation settlement charges rolled off the books.

In terms of the wildfire litigation facing BHE and its wholly-owned subsidiary PacifiCorp, Buffett and Greg Abel spoke at length about this issue during the annual meeting. Of particular note is something I wrote about last month — the Oregon Department of Forestry’s report that PacifiCorp did not cause or contribute to the Santiam Canyon fires tied to the James case, which has yielded multiple adverse verdicts so far. PacifiCorp has appealed these verdicts to the Oregon Court of Appeals — and has incorporated the ODF report into its opening appellate brief. Stay tuned.

In two separate, smaller fires for which PacifiCorp was judged to be responsible, the company has reached settlements with “substantially all individual plaintiffs, timber companies, and insurance subrogation plaintiffs”.

Manufacturing, Service, and Retailing

We’re always somewhat at Berkshire’s mercy as to what information we receive on the many, many operating businesses that make up this sprawling corner of the conglomerate. In Q1 2025, Buffett judged the entire MSR segment to be a “push” with net earnings virtually unchanged from a year ago.

Greg Abel revealed that he measures and follows 49 of these businesses especially closely — with 21 up in the first quarter and 28 down. “A mixed quarter,” he said.

Manufacturing pre-tax earnings fell 6.8% — dragged down by building and consumer products. Industrial products, meanwhile, remained flat.

Precision Castparts continued its resurgence with $2.7 billion in revenue and a 40.7% increase in pre-tax earnings. A combination of higher sales and improving manufacturing and operating efficiencies. There didn’t seem to be much of an immediate impact from the SPS Technologies fire back in February.

Lubrizol brought in $1.6 billion of revenue, but suffered a 25.8% drop in pre-tax earnings due to lower volume and selling prices — and restructuring charges.

Marmon’s revenues increased 3.4% to $3.1 billion, but pre-tax earnings slipped 2.4%. Seven of its twelve business groups posted lower earnings.

IMC’s revenue fell 3.3% to $1 billion on “sluggish customer demand across all major regions”. Earnings dipped even worse at 18.7%.

Clayton Homes grew revenue 7.4% up to $2.9 billion, though pre-tax earnings actually fell by $23 million (-5%). Clayton’s interest expense jumped up $99 million so far this year, as borrowings from Berkshire affiliates increased by $6.6 billion. Home unit sales increased 6.3% in the first quarter.

Elsewhere in building products, a 3.6% decline in revenue was primarily attributable to MiTek and Shaw. Pre-tax earnings of the non-Clayton part of the segment declined by 17.0%.

Over in consumer products: Forest River’s revenues were up, but earnings were down. Brooks Sports achieved higher revenue and earnings. Richline’s revenue increased on passthrough of higher metal costs. Revenue declined throughout the rest of the group — including Jazwares, Fruit of the Loom, Duracell, and Garan — due to lower customer demand.

Pre-tax earnings in the group sank 29.6% to $105 million. Fruit of the Loom did manage to eke out higher earnings thanks to restructuring and lower manufacturing costs.

Service and Retailing posted a 12.9% gain in pre-tax earnings.

Aviation services grew revenue 10.4% due to increased number of aircraft and flight hours at NetJets. Earnings increased, too.

IPS revenue increased 16%.

TTI revenue “increased slightly”, but earnings declined on lower margins caused by price pressure and for-ex effects.

The leasing businesses (XTRA and CORT) and Charter Brokerage (logistics service for petro-chemical industry) posted higher pre-tax earnings.

Berkshire Hathaway Automotive makes up 71% of the retailing group’s revenue — with home furnishings at 17%. BHA’s revenue jumped 5.3% (fueled by a 6% increase in vehicle sales and 6.7% in finance/insurance), though pre-tax earnings were “essentially unchanged”.

Revenue at home furnishings fell 1.4% — while all the other retailers combined suffered a 9.8% sales decrease.

Aggregate pre-tax earnings for the non-BHA contingent fell $24 million (-32.8%) year over year, though home furnishings stood out with an earnings gain.

Pilot’s pre-tax earnings rocketed 140% to $168 million, though its revenue actually declined by 16.6%. Asset dispositions and reduced interest expenses explain the discrepancy. Last year, Pilot took a $5.7 billion loan from Berkshire affiliates to pay off third-party borrowings and lock in a lower rate. Pilot still owes $4.2 billion on this.

McLane once again improved its margin — which led to a $16 million increase in pre-tax earnings even though sales declined.

Thank you, Kevin, for a thorough analysis!

You likely receive hundreds of pitches.

This isn’t one of them.

Hello @Kingswell,

Respect your work and what you hsve built here.

I am the Founder and Steward of the 100x Farm.

The 100x Farm is a quiet strategy sanctuary for investors and capital stewards with long memories and longer horizons.

No noise. No dopamine. No trend-chasing.

Just deep-cycle clarity earned slowly, shared rarely.

We don’t believe in inbox conquest.

But if the idea of sowing $10,000 seeds to harvest $1 million trees over 20- 30 years feels familiar,

you and your patrons may already belong here.

What if the next 100x isn’t a stock but a forgotten business model hiding in plain sight?

Every thesis is backed by real family capital, filtered through over 100 long-cycle lenses before it earns a word.

And if nothing else, this may help you filter what isn’t worth your time.

No urgency. No ask.

Only signal.

Should you, or your patrons, choose to engage, our farm door remains open.

Warmly,

The 100x Farmer