A Closer Look at Berkshire Hathaway's 2026 Proxy Statement

In just a few short pages, this filing celebrates Berkshire's unique culture and lays out the roadmap for preserving it long into the future

More than three decades ago, Forbes published an interesting article on the spiraling levels of executive compensation in the corporate world. The author took particular aim at Texaco — infamous for its lavish salaries and perks (though recently reformed) — calling it “a company run for the principal benefit of those who ran it”.

I think about that line every year around this time when Berkshire Hathaway releases its proxy statement. And how that filing makes clear, in just a few short pages, that Berkshire is run — and will be run — for the principal benefit of its shareholders.

Really capturing how Warren Buffett and Charlie Munger assiduously built the conglomerate in their own image. It both celebrates Berkshire’s unique culture and lays out the roadmap for preserving it long into the future.

The most newsworthy detail in Berkshire Hathaway’s proxy statement is the outstanding share count as of March 4, 2026. That just so happens to be the same day that Greg Abel and co. started buying back stock again after a nearly two year hiatus. By my back-of-the-napkin calculation, Berkshire repurchased 309 Class A shares for ~$225 million on day one of the recommenced operation.

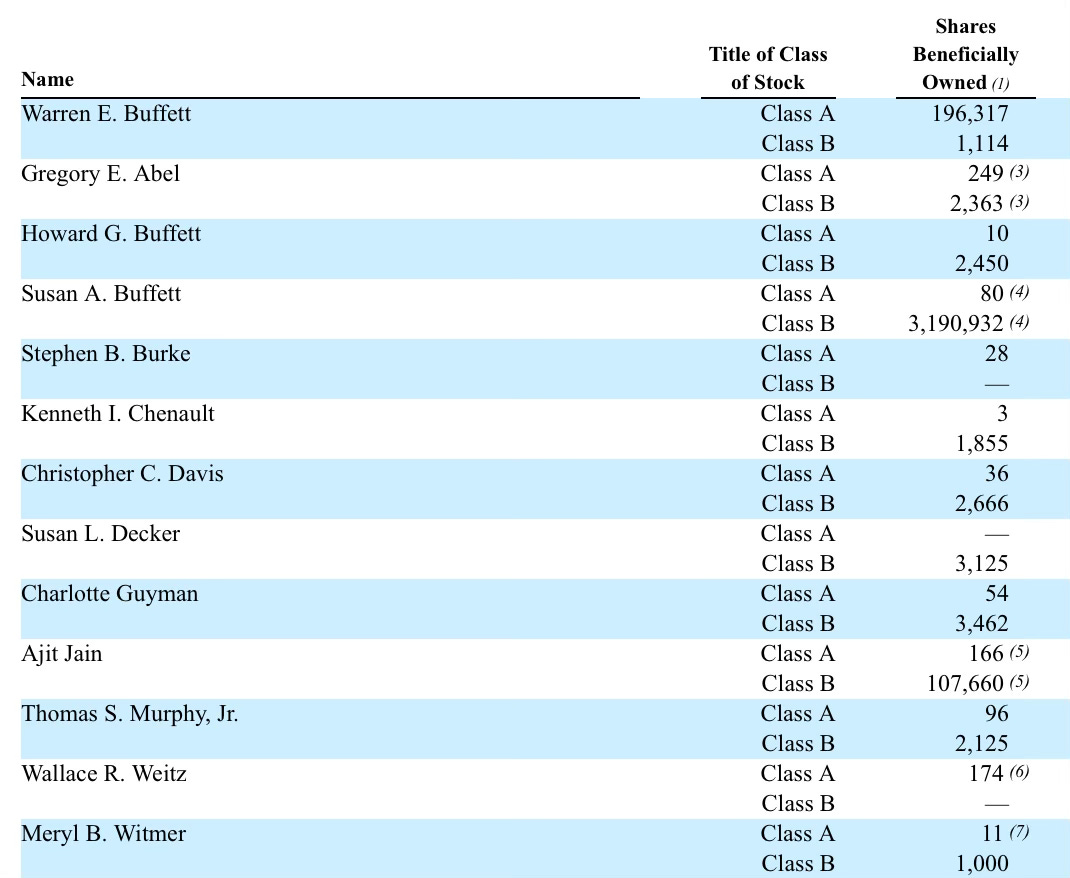

Warren Buffett might be retired, but he will surely remain Berkshire’s largest shareholder for the rest of his life. His stake represents 30.0% of the company’s voting power and 13.7% of its economic interest. (A year ago, his voting power stood at 30.4% and has barely budged despite ongoing charitable donations.) Whenever that sad day comes and Buffett shuffles off this mortal coil, he hopes that a family member will be named non-executive chairman. By all indications, that mantle will fall onto son Howard Buffett, who has served as a director since 1993. The proxy, however, makes clear that the ultimate decision on this rests with the board.

Understatement alert: “Berkshire’s program regarding compensation of its executive officers is different from most public company programs.” And that always started right at the top — with Buffett holding his salary steady at $100,000 for more than forty years despite leading one of the world’s most valuable companies. Greg Abel will draw a more conventional CEO salary of $25 million, but he has already publicly committed to spending every after-tax dollar of it on Berkshire stock for the remainder of his career. Skin in the game doesn’t get more serious than that.

Berkshire “never intends to use stock to compensate employees” — but loves writing big checks to top performers. As such, vice chairmen Greg Abel and Ajit Jain each earned $22 million salaries last year. The managers of Berkshire’s many subsidiaries also operate under incentive-laden compensation plans “dependent on such elements as the economic potential or capital intensity of the business”. These incentives can get quite large, but will always be tied to operating results within that person’s direct control. Buffett (and now Abel) alone was responsible for Berkshire as a whole, so tying anyone else’s compensation to its overall profitability or stock price would not be a fair reflection of their actual performance.

Berkshire does not, though, write big checks to its directors. The fee structure for the board is kept deliberately modest in order to attract only like-minded industrial exemplars who care deeply about the company’s future — and scare off those looking for a cushy sinecure to line their pockets. Berkshire employees who double as directors receive no extra pay, while the rest earn only $900 per in-person meeting and $300 per phone meeting. Members of the Audit Committee are the real high-rollers with an additional $1,000 each quarter. That means, for the full year, the highest-paid director made just $7,000 in total fees — with non-Audit members down at $3,000. It’s safe to say that Berkshire’s directors are not in it for the money.

Buffett has long warned about how lofty fees and perks can erode a director’s sense of independence and willingness to challenge the CEO when needed. No system is perfect, but Berkshire’s approach ensures that no one makes so much — or benefits to such a degree — from board membership that they lose sight of their role as stewards.

Perks are kept to a bare minimum. No company cars, no comped country club memberships, and no private jet trips for personal use. The proxy makes special note that “Mr. Buffett is personally a fractional NetJets owner, paying standard rates, and he used Berkshire-owned aircraft for business purposes only”. Berkshire’s model grants a fair level of cash compensation to proven performers, while insisting they act — and invest — like true owners. Circling back to the Texaco example that opened today’s newsletter, the oiler ended up overhauling its entire compensation plan in a very Berkshire direction with difficult-but-achievable incentives instead of perks. “If you want those things,” said Texaco vice president Carl Davidson, “we’re giving you an opportunity to make the money and buy them on your own.” I think Warren and Charlie would approve of that sentiment.

Berkshire seeks only exceptional candidates who align closely with its rigorous standards for board service. The Governance Committee evaluates potential directors against a clear set of attributes that Buffett considers essential “if one is to be an effective member of the board of directors”. Those being (1) very high integrity, (2) business savvy, (3) an owner-oriented attitude, (4) a deep genuine interest in Berkshire, and (5) a significant investment in Berkshire shares — relative to their personal resources — for at least three years. The committee noted that, in its judgment, all current directors fully embody these qualities.

A meritocracy above all else. Berkshire explicitly states in the proxy that it has no policy regarding consideration of diversity when identifying director nominees. “The Governance Committee does not seek diversity,” it reads, “however defined.” Instead, director selection will be guided solely by the consistent, timeless criteria set out above. Berkshire wants a board composed of exactly that sort of people — no matter what they look like or which boxes get checked. This has been the conglomerate’s stance for years, whether in or out of fashion, reflecting its principles-based culture that prioritizes competence and character over any demographic factors.

Berkshire will not bend on decentralization. There is only one shareholder proposal this year, which takes aim at the inconsistent approaches to “human capital management” across Berkshire’s many subsidiaries. In particular, it mentions labor trouble at NetJets and safety problems at Lubrizol. The board, unsurprisingly, urges shareholders to vote against the proposal — arguing that an overarching framework across all subsidiaries would defeat the purpose of decentralization. Decisions of this kind are best made by the people closest to the business, not a suit sitting in Omaha. Decentralization is a feature, not a bug, at Berkshire Hathaway.

We need more companies to be like this. Less and less shares. Only competent people paid for performance

Kevin, you summarize well why Berkshire has a very large Margin of Trust.